Dollar General: Opportunity or Trap?

Dollar General: Opportunity or Trap?

Bull, Mid, and Bear Case Scenarios

The Business

Dollar General operates small box stores - 19,726 of them and growing in the US.

Selling everyday consumables such as food, snacks, health and beauty aids, cleaning supplies, basic apparel, housewares and seasonal items at everyday low prices in convenient neighborhood locations to lower income $40k or less households in the western and rural parts of America, DG over the past 20 some odd years developed a supply chain system and network of small stores to service the people big box stores like Walmart and Costco cannot (economically) and will not (strategically) serve.

Doing so has been tremendously value accretive to shareholders up until the recent -45% in share prices. Pre 45% meltdown in share price, the returns an investor could have gotten outside of dividends would have been almost 1000%.

Post melt-down, CAGR for the starting investor in 2009 (ex-dividends, which is significant) would stand at 13.26%.

I’m using very rough numbers here to show that despite a large drawdown, an investment in the company was an overall solid choice if you had the ability to see past its unsexy business model.

Which begs the two following questions:

Why did Dollar General shares tumble? Is this a business model failure or a bump on the road?

What are the expected forward rate of returns for investors who are willing to look past the current problems and invest at $129+ per share?

Business Model

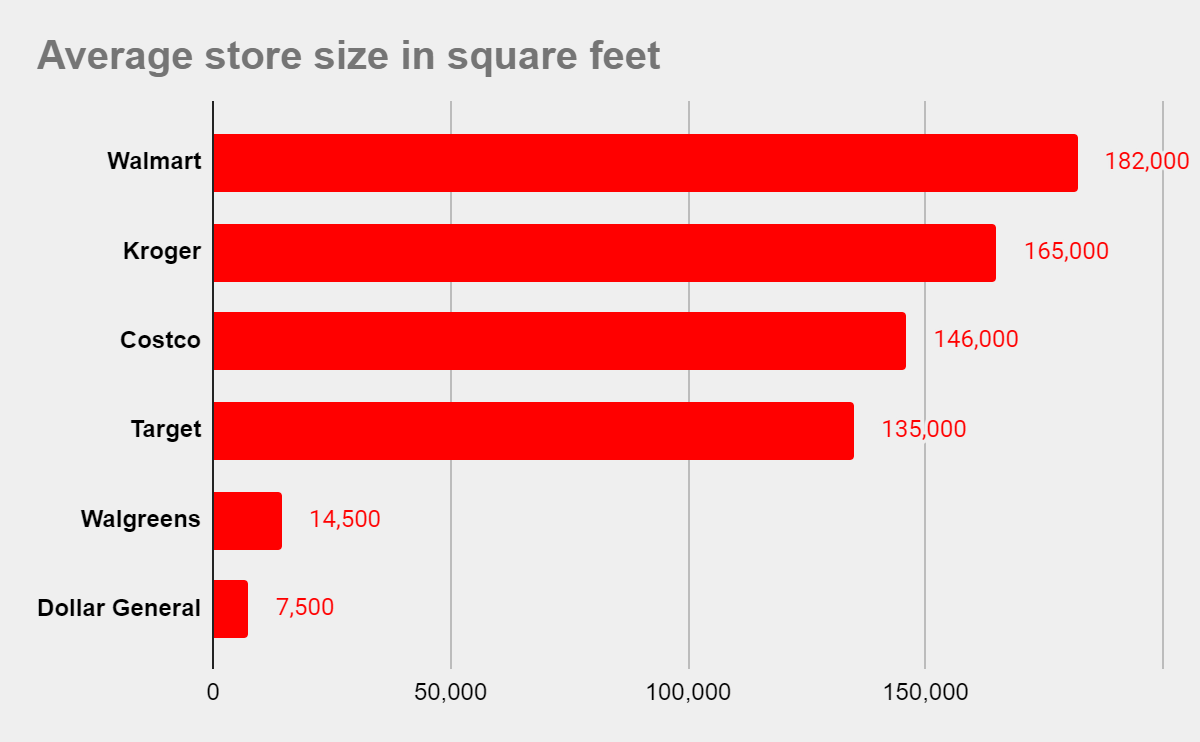

Some of the biggest and best national retail chains that anyone can recognise like Costco’s average 146,000 sq feet) or Walmart’s 182,000 sq feet). Dollar General’s average store size for comparison is only about 7-10,000 sq ft.

Direction determines destination.

The disparity between how big box retailers and Dollar General operates is useful to understand because it allows us to understand two extremely important ideas:

The source of Dollar General’s moat.

The direction of Dollar General’s moat.

In the early days as retailers sought to quickly gain ground and market share, greater product ranges, cheaper prices, and more convenient central city locations were the main competing metrics.

It made monetary sense too.

Its cheaper to push a large amount of goods across to one store and have it be the central hub of sales versus run your fleet up and down the country dropping a tiny portion left, right and center.

You don’t have to be a genius to figure that supplying and maintaining a single source of distribution is cheaper versus doing it for thousands of tiny stores spread out over a whole country.

But inversing is a valuable idea.

While the big box retailers slugged it out, competing on SKU diversity, shopper comfort, lower prices, and quality products (all the while burning valuable capital), Dollar General realised very quickly that they could simply go where no one else would and earn a decent margin.

The difference in operating margins is telling even to this day.

Double Whammy of Earnings & Interest Rates

We know the move worked (reference the above share prices and margins) - so what caused the most recent share price meltdown?

Comparing their quarterly reports:

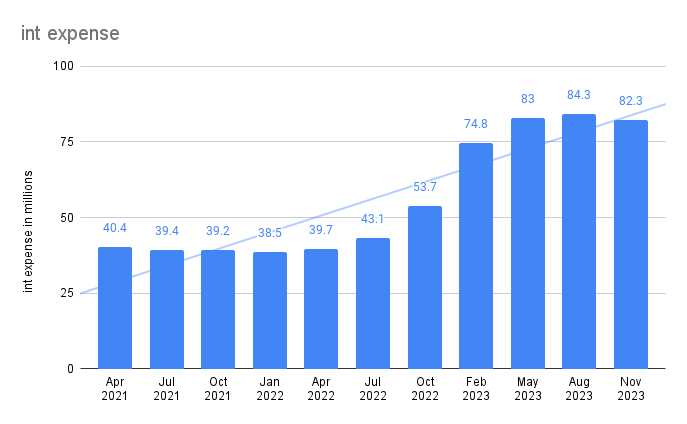

Interest expenses are up almost a 103%

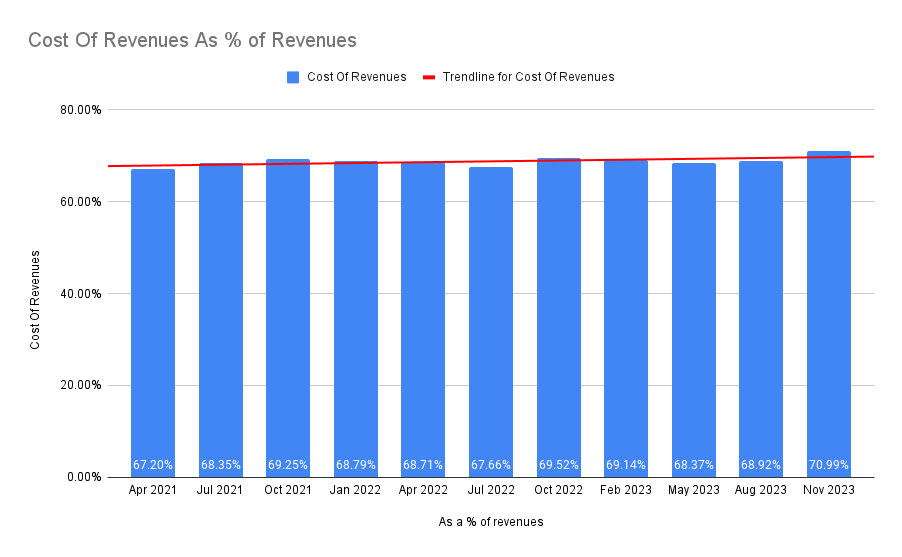

Cost of revenues as a percentage of total revenues has climbed

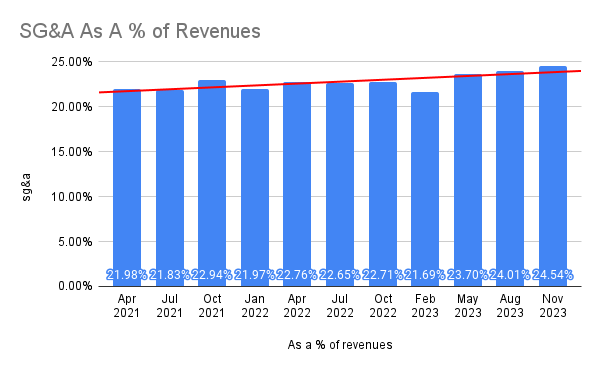

SG&A as a percentage of total revenues has climbed

SG&A as a percentage of total revenues has climbed

All businesses are margin businesses, but retail has especially slim margins. Dollar General’s earnings are suffering from combined pressures on both ends:

In a short 2 years:

SG&A has jumped 11.64% v Apr 21

Cost of Revenues has jumped 5.64% v Apr 21

That is what has led to a outsized decrease in net income. I’ve included numbers from Apr 22 to get a better sense of the numbers.

Can They Turn Around?

The turnaround actually isn’t that hard.

Retail is about operational discipline, and while certainly the above numbers seem to indicate that its hard, Dollar General’s history seems to indicate that they have had some experience running a tight ship.

Some things I’ve gleaned from most recent management comments.

Operational discipline has become a problem at some distribution centers. this will take time to fix.

They are reducing the range of SKUs deliverable to stores and marking down then selling the rest. I expect better ROI on fuel, time, and labor from these initiatives.

Increasing manhours to keep stores clean, well stocked, and communicating properly to distribution centres for restock is key. So I’m all for it if it keeps stores humming along in sales.

So can they turn things around? I’m not 100% certain. But I think they have a better chance than most and with the back-to-basics push by CEO Todd Vasos.

What Drives Forward Returns for Current Investors?

Per its latest quarterly report, average sales per square foot for all stores over the 53-week period ended November 3, 2023 was $270.

Based on $39,036 TTM reporting revenues and $270 sales per square foot, we’re looking at approximately 144,577,778 of selling square feet.

If we divide 144,577,778 square feet by the average 7500 sq feet space of a single dollar general store, we get 19,277 stores

This checks out with the reported 19,726 operating stores per their most recently quarterly.

Assumptions:

600 new stores per year between now and next 5 years till 2029

Sales per square feet remains stagnant at $270

On a PE basis

Assuming share counts stay the same and baking in the above, I’ve tabulated what 17x PE and 20x PE will look like.

Returns look decent if Net Income Margins can recover from its current 2.85% to 6+% over the next 5 years w a return of 9.79% average. It goes up to 13% at 7% NI margins, and 19% CAGR at 9% NI margins based on 17x PE, which isn’t too far from its current 16x.

If management executes on the logistics end, macroeconomic climate recovers, inflation slows down and interest rates all go down at the same time, I think its not too hard to see PE multiples of DG trade back up to 20x and for the share price to go higher.

Note these calculations are all based on smaller than average store expansions based on provided quarterly reporting data, and also excluding any dividends or share buybacks.

Including those factors in, I think it’s much more likely to see a higher rate of return in DG at current share prices and I am a net buyer.

What I Haven’t Liked (though I’m Biased)

Capital allocation decisions:

Paying down debt is attractive here as well with interest expenses up 87% from Apr 21. We can see that reflected in share prices without having to pay Uncle Sam 30% taxes along the way.

Share buybacks form the other more efficient means of shareholder return. All else equal, if no further cash can be applied judiciously towards expanding store sales footprints and reinvesting in the moat, then I would prefer the company to buyback shares instead of return it as dividends. Aggressively shrinking shares o/s have done AZO wonders. And I’m fairly certain the same can be repeated here.

Diworsification: Pop-shelf concepts - I’m not sure how to feel about popshelf concepts. Of course, I’m not privy to company internal ROIs but I’m hoping to god this doesn’t become something that DG spends valuable time, money and effort on only to rescind it later on for naught.

Margin tailwinds

Fresh food consumables - DG has been accused of causing food deserts in the past via moving in and causing local grocers to die off. [I note with curiosity why no one is questioning the consumer here for buying only from Dollar General…is it perhaps that grocers don’t provide sufficient value to stay in business?] Any move made by them in the process of such elimination in boosting fresh food availability [often as the only game in town!] sounds good to me.

Reducing SKU count, improving supply chain productivity and On Time and In Full deliveries to stores.

Inventory turnover accelerating after investing in labour.

Reduced theft from improved labour.

Embedded Low Probability Call Options for Shareholders

Literally anything else that allows Dollar General to make use of its hardened, efficient logistics network

How I’ve Traded It So Far

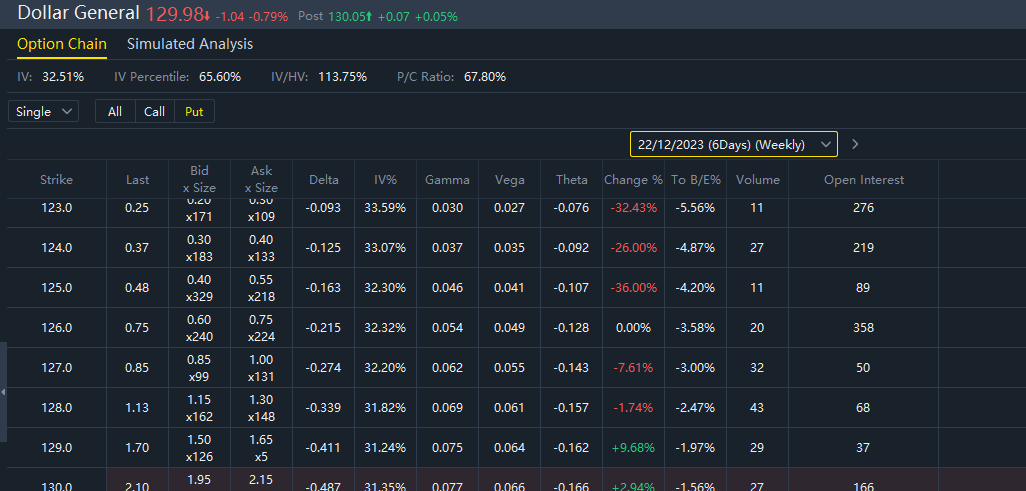

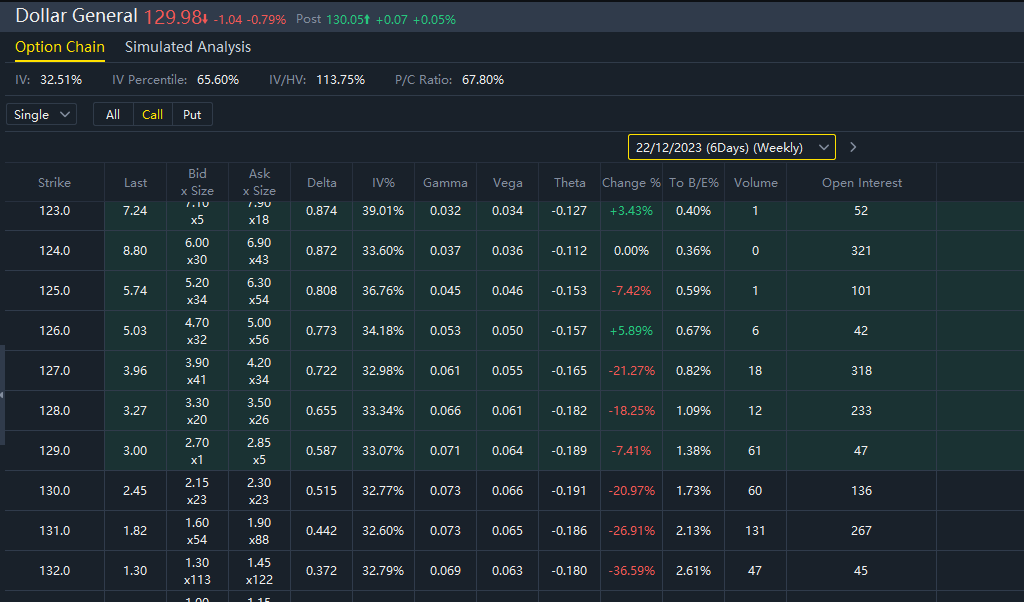

I bought 400 shares of Dollar General at $134.86 then immediately sold calls at $5.24 credit per share. That reduced my effective price to $129.62.

Calls expired worthless (I kept $5.24*400 = USD$2096) when earnings came out and topline grew but margins remained lacklustre.

Since my average was $129.62, there was nothing to lose selling a new set of 4x calls at $129 strike with $1.27 premiums. Bringing my average down to $128.35.

Shares were called from me as of last Friday with the stock trading at $130.05 after hours.

The net result is that I’ve earned USD$260 from my position in a matter of 2 weeks and most importantly, I managed to rigorously protect my downside while maintaining my upside.

There’s nothing stopping me from buying 400 shares of Dollar General (at $130.05 versus the $134.86 to boot!!!)on Monday.

Based off current market option chain pricing, I can sell $129 strike puts x 4 for $600 ($1.50*400) and let it be assigned to me if it drops by Friday…

Or…I can do the reverse. Buy shares, sell calls against it for 131 at $1.60*400 shares for USD$640.

Or I could just buy shares and sit. Either way, I think there’s a genuine opportunity here and I’ll probably remain a net buyer of shares while looking to reduce my downside through sell otm calls on a week to week basis. I’m not certain of course that it will work out better - it might be that the best play is to sit on the shares and do nothing (in which case I’d be down -2.9% now).

I hope this has been helpful anyway.

Good luck.

And remember - this is not investment advise. Dyodd.