Why I Bought Autozone

Disclosure: I am long, obviously. This is not investment advise. Please perform your own due diligence. I am not compensated for this article.

Edit: I’ve recently been alerted AZO does not in fact provide repair services in house but will instead furnish consumers with all of the materials so that mechanics only need to charge for labor. (a sample of understanding this dynamic can be found here: https://outofyourrut.com/how-autozone-made-me-a-customer-for-life/). Note t

I bought Autozone recently. I’m going to briefly go over the key metrics below then we’re going to dive into the business specifics and why I’ve bought it.

Operating Metrics

pre-tax income (2020): $2b

mkt cap: $26b, or approximately 13x pre-tax earnings

free cash flow per share: $96

price per share: $1179.74

p/fcf: 12x fcf, fcf yield of 8%

roic historical 5Y avg: 23%-35%

Return on Incremental Invested Capital: 80+% (refer below for calculations)

Business Description

AutoZone, Inc. retails and distributes automotive replacement parts and accessories. The company offers various products for cars, sport utility vehicles, vans, and light trucks, including new and remanufactured automotive hard parts, maintenance items, accessories, and non-automotive products. Its products include A/C compressors, batteries and accessories, bearings, belts and hoses, calipers, chassis, clutches, CV axles, engines, fuel pumps, fuses, ignition and lighting products, mufflers, radiators, starters and alternators, thermostats, and water pumps. The company also offers maintenance products, such as antifreeze and windshield washer fluids; brake drums, rotors, shoes, and pads; brake and power steering fluids, and oil and fuel additives; oil and transmission fluids; oil, cabin, air, fuel, and transmission filters; oxygen sensors; paints and accessories; refrigerants and accessories; shock absorbers and struts; spark plugs and wires; and windshield wipers, as well as air fresheners, cell phone accessories, drinks and snacks, floor mats and seat covers, interior and exterior accessories, mirrors, performance products, protectants and cleaners, sealants and adhesives, steering wheel covers, stereos and radios, tools, and wash and wax products. In addition, it provides a sales program that offers commercial credit and delivery of parts and other products; and towing and tire repair services. Further, it sells automotive diagnostic and repair software under the ALLDATA brand through alldata.com and alldatadiy.com; and automotive hard parts, maintenance items, accessories, and non-automotive products through autozone.com. As of August 29, 2020, it operated 5,885 stores in the United States; 621 stores in Mexico; and 43 stores in Brazil. AutoZone, Inc. was founded in 1979 and is based in Memphis, Tennessee.

Business descriptions are wonderfully helpful things.

What can you glean from the above description of the business? Think about it from an owner’s perspective, about operating it, about putting your money to work on it, about how you’d try to make some income with it.

Several things should immediately stand out to you.

High capital intensity: There is an extensive variety of car parts and car repairs/models/makes on the road that require servicing -> this means as a person in the business, you need to carry those parts on hand to make repairs asap (because car repairs often can’t wait) and you need to have ALL of those parts because if I go into your store and can’t find a part, I’m unlikely as a car owner to ever go again.

When capital intensity is a factor in the business and inventory is involved, always look at cash conversion cycles (CCC) and scale.

Scale begets bargaining power which begets a negative cash conversion cycle which begets a business beginning to hit “escape velocity”. Once you can serve the incremental customer as a physical business without running out of cash, it becomes much easier to push the next 1000000 customers with space, location, and store expansions/online infrastructure becoming the remaining “bottlenecks”.

Note this obviously has a ceiling since you cannot squeeze margins on suppliers infinitely and you cannot maintain irrational price hikes year over year or you risk losing consumers to more competitively priced alternatives - although this does give the business some form of pricing power, and a very limited one at that, most of the pseudo-pricing power comes from negotiating lower costs from suppliers and longer payment terms.

tl; dr, focus on scale, cash conversion cycles, physical store locations + online traffic driving/in store fulfillment to drive sales growth as a capital intensive business owner. Almost all retail stores are doing this: Walmart, Costco, Target, Dollar General. It makes sense even for a cousin industry in Autozone to do this as well. Hence, for this business, distribution, scale, bargaining power w suppliers, are all moats.

How Does Autozone’s Protect It’s Returns on Invested Capital?

*Autozone will be referred to as AZO from hereon.

The golden rule of any business is that it needs to make money. No shit, right?

Yet today, we see people pushing 20x price to sales ratio on businesses w no demonstrable ROIC .

This metric, for those more uninformed is called return on invested capital (return on invested capital, short form ROIC).

If you shell out $5 million today to set up a burger store, hire staff, pay suppliers, do some marketing, cover overhead expenses, pay off lease obligations (rent), and you net $1 million at the end of the first year - that’s a 20% ($1m/$5m) roic business. And what a great business it is!

What that really means is after 5 years assuming no growth and no drop in sales, the business pays for itself and all cashflow from year 6 moving forward to year 100 is “free”.

That’d be a pretty awesome thing wouldn’t it? To have an asset that just keeps churning out $1m every year from year 6 to year infinity?

But hold up —> 20+% roic isn’t easy to get.

Most businesses are lucky to average 5-8% ROIC, implying they earn $5-$8 for every $100 of capital. What that implies also, therefore, is that every investment in a business w roic of 8% is basically accepting a longer “payback” period.

To understand why 20+% returns on invested capital is spectacular, consider that the S&P500’s average ROIC at end 2019 was 8.2% (which is pretty decent!), and further consider that the market average roic for listed companies ranges between negative (they lose money!!) to 6%.

Then you have the middle tranches of profitable companies occupying the range between 7%-15%, and the truly astounding businesses averaging 15% - 30+%.

Herein lies the rub. High returns are noticed and very quickly, when able, taken away by new entrants and new competitors.

A significant advantage must be held by the first burger store in order to stop further burger stores from muscling in. This can be via a multitude of ways, and Pat Dorsey in his book (the Little Book that Builds Wealth, I highly encourage reading it) has done a great job explaining what most of them are.

And that is perhaps what makes Autozone great. It has averaged returns on invested capital of 20+% for the better part of a decade.

That begs the question:

(A) how has AZO maintain its high returns on invested capital? (what is it’s competitive advange/Moat?)

(B) how does it stop competitors from doing the same?

(C) is it at risk of being threatened anytime soon?

My firm belief is that 90% of the work of any prospective investment is meant to be focused on the above questions combined with a deep look at executive compensation. Management matters, and idiots can always run a great business into the ground.

In this regard, Autozone fulfills most, if not all of the various things I look for in a business I wish to hold forever.

It’s competitive advantage is not easily replicated.

It achieved scale and negative cash conversion cycles significantly ahead of industry peers and thus enjoys a head-start in the race for market share.

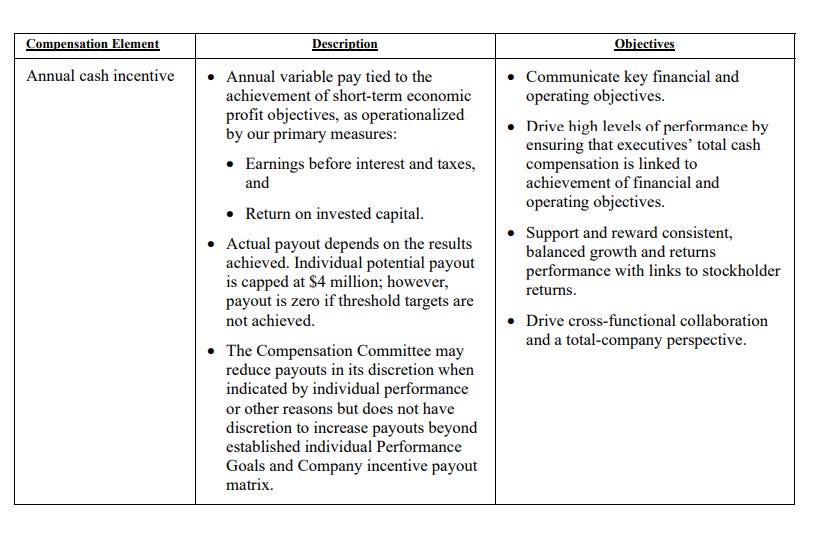

Management is compensated for raising returns on capital and punished w lower salaries for lowered returns on capital (90% off CEO pay is tied to returns on invested capital, 78% average of all other officers the same).

Reinvestment opportunities - AZO’s revenue as the auto industry leader is a mere 10% of the total addressable market. Incremental invested capital, whilst having to be deployed slowly/carefully, has averaged nearly 80%. (2016 adjusted after tax return was $1,518,890 compared to $2,148,173 for 2020. Invested capital was $4,860,021 in 2016 compared to $5,641,533 for 2020. In other words, an increase of $781,512 for invested capital produced an increase of $629,283 in after tax earnings, or approximately 80%!!! *Note that the increase in capital invested is merely 8% of all after tax earnings over the past 5 years, so whilst the return is great, the rate of it is slow).

Note that the industry is basically oligopolistic with top three players (AZO, O’Reilly, AAP) accruing most of the profits. As of Sep2020, a Bank of America study puts respective market share for the auto-parts industry at Autozone (14%), O’Reilly (9%), Advance Auto Parts (6%).

Autozone’s Scale Flywheel

How does AZO protect its moat?

AZO hit the scale level from which it could engineer “escape velocity” before everyone else in its industry could.

What am I talking about?

Generally speaking (although not always true), scale allows larger players to delay paying suppliers while advance asking for payments.

Further, consider the demand Autozone serves: car parts are mostly (some % of sales are discretionary) a non-discretionary market. If your car breaks down, you can’t push back fixing it to next week or month or year. You fix it right away.

This, plus the fact that payments are consumers on the ground and not another business mean that DPO and DSO should be wide enough to allow $AZO a pseudo negative working capital business.

This dynamic is only possible because (a) auto parts manufacturers are in the commodities business and a commodities business is in the volumes business - low margins means you MUST sell bigger volumes to generate even slight profits.

This means you’re more likely as a supplier to like and want to do business w a larger scaled partner like Autozone and would even offer lower prices to retain clients - bargaining power lies w Autozone the bigger it gets.

Coupled w the fact that no one waits to fix their car, Autozone is able to leverage a negative working capital business model to efficiently scale vs its competitors whilst slowly consolidating the gigantic autoparts industry ($360 billion estimated globally)

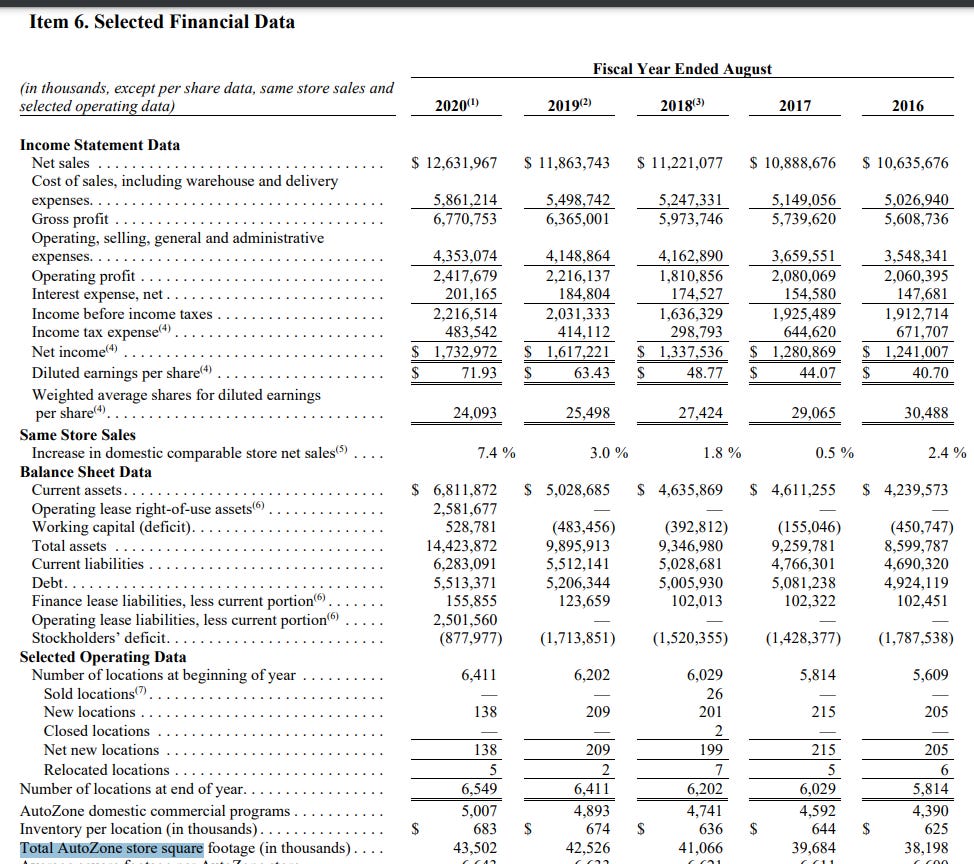

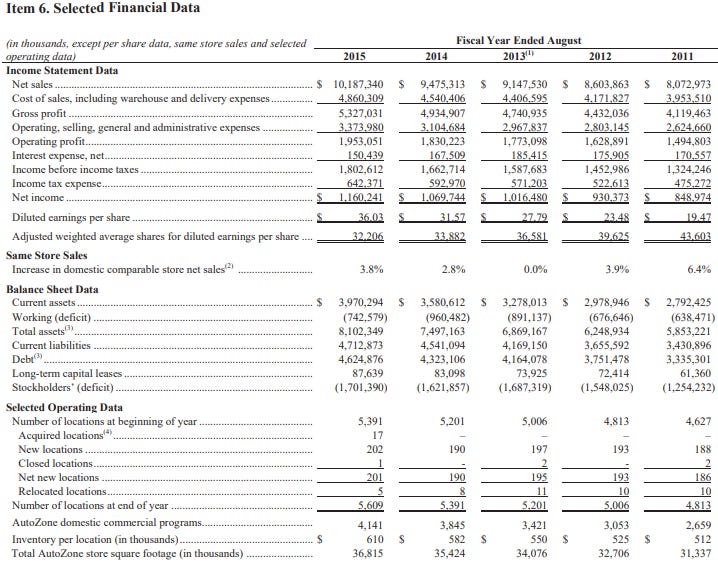

AUTOZONE

While this might seem like a small edge, trust me when I say it is not. Revenues for the past 3 years totals up to nearly $45b, averaging about $11b-$12b per year.

I can’t imagine having to carry $11-$12b per year of extra inventory on your own balance sheet as anything but an albatross around your neck. Inventory you don’t sell is inventory you have to keep on the books. That’s $11-12bn you can’t use to build out routes, build new store locations, hire more staff, etc cetera. If business is war, cashflow are the bullets you fight it with.

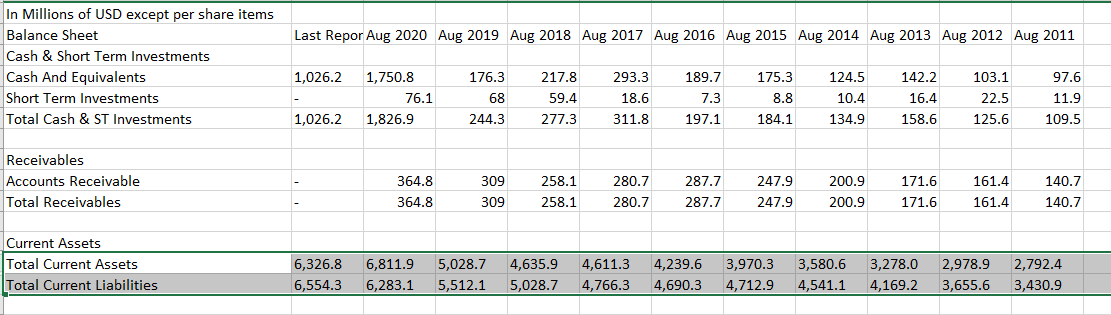

Here’s a look at O’Reilly’s and AAP’s sheets.

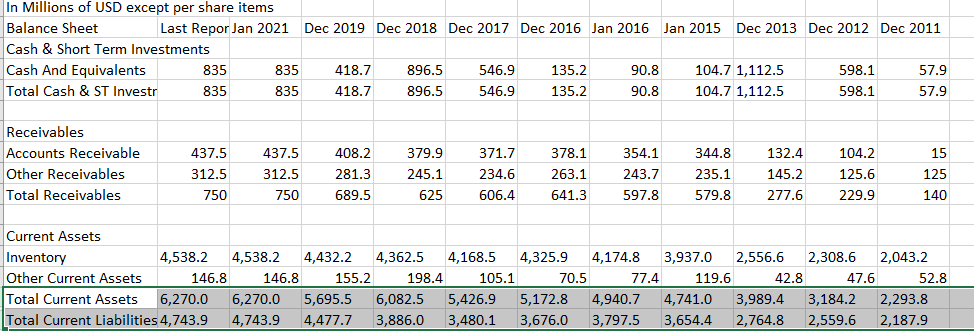

ORLY - O'Reilly Automotive, Inc.

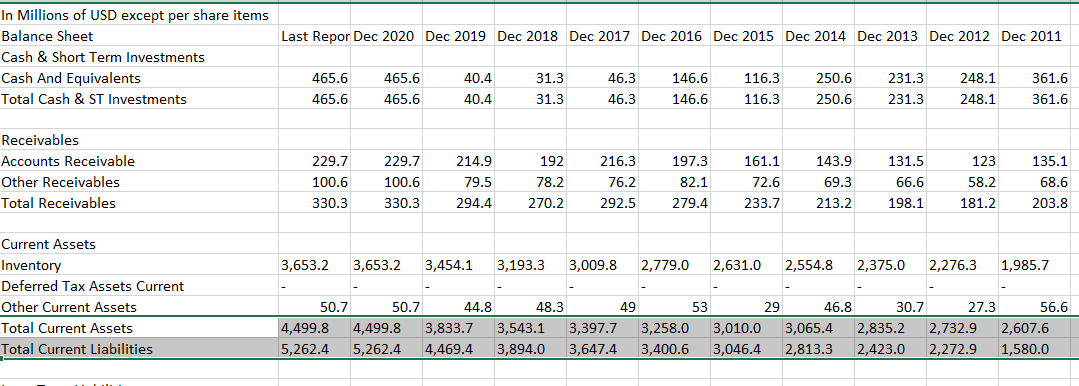

AAP - Advance Auto Parts, Inc.

It’s telling to me that the two companies with greater market share is able to employ negative working capital to further entrench themselves.

The above effect I’ve described can otherwise be seen as a number called the Cash Conversion Cycle (CCC).

CCC’s formal definition:

The cash conversion cycle (CCC) is a metric that expresses the time (measured in days) it takes for a company to convert its investments in inventory and other resources into cash flows from sales. Also called the Net Operating Cycle or simply Cash Cycle, CCC attempts to measure how long each net input dollar is tied up in the production and sales process before it gets converted into cash received. ~~(link)

Here are AZO, ORLY, and AAP’s CCC respectively across the years.

AZO

ORLY

AAP

To clarify, negative cash conversion cycle simply means that Autozone will in effect never be out of money to sell greater amounts of products - an advantage normally ascribed to digital only businesses.

This also means that AZO was able to serve the incremental customer at its various outlets and stores without incurring extra costs since 2011 (of note, AZO’s 2011 ending share price was $324.97, the price of a single share of AZO today is 1179.74, an approximate 2 bagger over 10 years. Put another way, a holder of AZO’s shares would’ve seen his share compound value at 13.76% every year since 2011.)

2011 - 2020;

Total AZO store square footage went from 31,337 to 43,502 (27% increase), net sales ($288) per autozone square footage has largely remained similar, which means expansion in stores/sq footage drives earnings growth.

Total ORLY (closest, largest competitor) store square footage went from 26,530 to 40,227 (51% increase), net sales per sq ft went from $221 to $255.

All in, the differences here are minute except for valuation. $ORLY trades at 16x pre-tax earnings, and $AZO at 13x. I’m inclined to go w the cheaper company all things withstanding given that both remain two of the pillars within the Auto-parts industry.

Inventory turnover, which effectively measures how long inventory sits on shelves doesn’t bode anything out of the ordinary as well.

AZO: 1.33

ORLY: 1.55

AAP: 1.25

This translates to an average time-on-shelf for inventories of about 9 months for AZO/AAP and about 8 months for ORLY. (12 months/inventory turnover rates). Overall, no real disparity.

Threat of New Entrants

Amazon, Walmart, Target

We can’t really talk about AZO/ORLY without first looking at the giant pink elephant in the room. High margin businesses have become victim of late to Amazon’s (AMZN) ever encroaching, low margin, high fulfilment business. As AMZN continues to leverage its huge network of increasing consumers to spread out fixed costs and achieve a bigger scale flywheel, it will inevitably encroach upon AZO’s discretionary, and other items with low user expertise required (ie; installing and wiring a computer requires more significant expertise versus plugging in a bluetooth).

As of latest report, discretionary and maintenance items were still the smallest portion of AZO’s business.

I fully anticipate a larget portion of this to be eaten away over time by the entrance of Walmart & Amazon. But I assign almost no existential threat posed by naysayers of AZO and the market in general.

Before I’m branded a charlatan with a blanket statement, consider the evidence the world has offered. YouTube and Google has been around for at least a decade.

Information and knowledge on car parts and car repairs can be freely found on the web.

In addition, whole zones including Facebook groups, reddit threads, discord servers and hardware forums all have discussions about after market products such as protective paint, carpeting, wipers, windshield wiper fluids.

Question:

Why, despite the proliferation of knowledge and lowered cost of access has consumer need to expertise mechanics and repair aids gone up instead of down?

Why has the public not self-diagnosed, self-repaired most self-solvable problems that doesn’t involve lifting your engine out of the car or lifting your car on struts to check the underneath?

Hell, before I even continue, let me ask you a question.

Do you drive?

If your car failed, would you google the answer yourself, buy the part, install it, risk doing it wrong and voiding your insurance whilst spending half a day or pay the local mechanic a visit? If you DO pay the local mechanic a visit, would you rather pay more or less? Autozone can furnish you the parts at cheaper cost and allow you to only pay for labor.

Beyond that, let’s continue with two ongoing “macro” trends which might serve to answer this why sales related to “failure” and “maintenance” has not gone down.

Modern jobs require greater domain expertise, and therefore, greater domain commitment: People are now required, more than ever, to develop deep domain expertise on their chosen job focus. If you’re a coder, you might have been tasked to learn more than one programming language. Does this leave much time for you to understand how to fix and solve car problems? Perhaps not. I could see a situation where a part time car enthusiast coder could get the job done, but even then, time is of the essence. You don’t pull into your home to fix a problem 90% of the time unless you’re absolutely certain you can fix it. You pull into Autozone/a mechanic’s shop and have them do it for you - the cost is too great not to. Notice the above trend plays out to analysts, bankers, doctors, engineers, academics, plumbers, etc cetera. In almost any job sector, deep domain level expertise and experience is rewarded with greater pay/roles.

Cars are becoming increasingly complicated: Rear sensors, side and rear cameras, self-driving features, advanced alarm systems are mostly unique and differentiated by brand/feature/pricing/manufacturer. Does the average consumer have the knowledge, access to tools, and ability to fix a malfunction? I don’t think so.

In sum, whilst I think it is natural for Amazon and other competitors to eat away at low-cost, low-expertise discretionary item margins, Autozone and ORLY among other deep domain expertise level niches will continue to deliver greater value to consumers - consistency in fixing an immediate and urgent problem will always triumph.

I could charge triple the rate to fix a person’s computer today and if it was mission critical, they would happily pay to have their systems up and running. This is the salient qualitative aspect AZO/ORLY is party to that bears are not pricing in.

Threat of Electric Vehicle

Let us consider the topic of Electric Vehicle as a threat to AZO/ORLY’s business. (A) bears say that EVs have far less parts and therefore far less need to be serviced/repaired/maintained and invariably leads to lower margins/returns for Internal Combustion Engine oriented servicer/fixers.

I’ve reviewed most of the “evidence” presented by bears and checked with electrical engineers, autoparts mechanics, whilst referencing reports among other data. All evidence points to 3 salient factors;

There is a perceived difficulty in getting charges as and when needed as an EV driver. While I’m certain I can drive into a local gas station, I’m not so certain I can drive into a nearby charging station nation wide in the States.

EV have less range and generally costed more. But there’s a curious pattern of EV automakers only insuring 70% of battery costs. Is a mission critical, expensive piece of equipment something you’re willing to accept 70% insurance on as an EV driver? Most logical people would say no. And costs, insurance, access, efficiency all pile up.

Incentives have not changed. Until the world over starts financially incentivizing electric vehicle usage (lower taxes, higher rebates, greater insurance coverage enforced at the Federal level, increased government support, improved EV charging infrastructure), I do not believe human behavior towards conventional ICE vehicles will change. Generally speaking, the everyday man on the street exercises great caution choosing a vehicle - and the facts point towards a typical ICE car, not an EV as the preferential choice.

Tailwinds

There are three current tailwinds I believe drive AZO’s earnings and value accretion materially higher in the next one to three years.

First, a downward swing in jobs, expected salaries, increased commodity prices, and inflation will force greater cost-conscious decisions across the board for consumers. This trickles down from car buying to maintenance. Historically, recessions and bad job markets have been good for AZO.

Second, the average age of light vehicles (cars, trucks) have risen to 12 years in the US. This leads to greater small amounts spent on maintaining a car vs buying a new one. Whilst seemingly small, consider that there might be upwards of 100 million cars in the US over 10 years of age in the next 4 years. The average cost of maintenance for a car nearly triples from 3 years of age to over 10 years of age.

Third, consumer focus is increasingly on quality and duration of value an asset can bring. No shit, right? Everyone wants a car to last longer - especially when they pay big bucks for it.

So the valuation makes sense, the company has a moat, tailwinds trump headwinds. What we have left to evaluate, is capital allocation and executive compensation. This article has been lengthy, so I’ll try to make it quick.

Excellent Capital Allocation

Autozone is a serial share eater. What share buybacks do, contrary to the damning manipulation certain US senators believe is that it increases the average earnings each share has access to. When earnings per share rises, so does value. And when value rises, so does the wealth of shareholders.

By buying back stock at opportune moment, companies deliver greater shareholder wealth and value. That is a net good. AZO has demonstrated that a cashflow gushing machine properly allocating capital to share buybacks at opportune moments can absolutely deliver blowout shareholder returns.

Executive Compensation

I’ll paste a screenshot and let you figure out if 90% at risk compensation for the CEO is a good thing or not.

Culture

AZO also enjoys a good reputation from excellent customer service which is prevalent across most of the customer review platforms that I could find online. Perhaps this it a sample sized bias, but experiences such as the one below isn’t something I can say is the norm for most businesses the world over.

That AZO can do such a thing at its size and get the culture (which isn’t as important as ROIC, yet important nonetheless!) right down to the customer experience/ground floor sales staff is an achievement for a $26.40B company.

Summary

Here’s the shorthand for those of you lazy to read through the whole mess above.

AZO and ORLY are both leaders in the category, but AZO trades cheaper at 13x pretax earnings vs ORLY’s 16x. Both have hit “escape velocity” and will continue to use scale as leverage to extract greater price reductions from suppliers and higher prices from consumers.

Threats are overblown. A detailed examination of what I could find suggests that EVs will really only be able to “take over” greater market share over the very long term. There remains a huge incentivization/structural issue to resolve for AZO’s main market, the US, to be heavily affected by EV penetration.

Capital allocation is stellar and return on incremental capital allocated is extremely high. What remains if often dedicated to share buybacks.

AZO enjoys counter-swings from recessions and general industry tailwinds that have not been priced in. I believe this will at some point, increase earnings while driving modest multiple re-ratings.

The two points above this means that we have above average “upward momentum” when there is “calamity” in the markets. Like my Berkshire thesis, AZO remains happily able to repurchase massive amounts of shares when it is presented with an opportunity to.

Culture is a pleasant to have sign that leadership is setting the right example. Customer service is what sets apart businesses in an essentials/commodities industry.

I’ve left out domestic commercial programs/deeper dives because I have been unable to scrape more information and specifics on this.

Disclosure: Long. This is not investment advise. Please do your own due diligence.