Trade for 13th November: Crowdstrike and Why

Trade for 13th November: Crowdstrike and Why

Results for 10th November Trade

Apologies for irregular updates but:

I’m recently married

Proposed, did the wedding, bought the house, went on a honeymoon, currently in the process of moving in

As you can imagine - the above events soaked up a majority of my attention and time.

I am now however freed up to continue writing - so here we are.

Updates from Option Spread Trading

Option spreads trading doesn’t work well. Or maybe I’m just bad at it. In theory, a spread entails a short call/put option and a long call/put option combined to protect your downside. Your maximum risk is capped since your long side covers your short side, and your maximum reward is the credits derived from your trade.

In practise, volatilty, expiry timing, forced assignments, and using out the money options to force trades and close short positions all come into play. Between all of these are trading fees, and the losses can really be 2-3x what you expect since the fees are applied at a per contract basis. My losses weren’t great, but the trades left a bad taste in my mouth. I’m closing this side of the options playbook to return to simple measures.

7th November Trade:

Sold the puts on a Tuesday since on Monday I was still in Japan and effectively wrecked after a full day touring USJ. 20,000 steps on not so good legs knocked me out hard.

Sold 3x 190 CRWD 0.00%↑ puts for $2.60 limit

Was ok being assigned. Was ok not being assigned as well. This is critical.

As usual with my core philosophy in using options as they were designed and not as gambling parlor greek tricks - I am fine with holding the underlying shares for 5 years or more in the event of a market shutdown (though I think if there merits such an event, we would all be extremely nervous about nuclear fallouts versus stock prices).

This option expired worthless as of 10th November - the day of my return trip from my honeymoon in Japan.

ComsonedPric 3Lot(s) Average illed Price FilledAmount Filled Amount 2.60 Time force 780.00 Currency ency Valid for the day USD'")

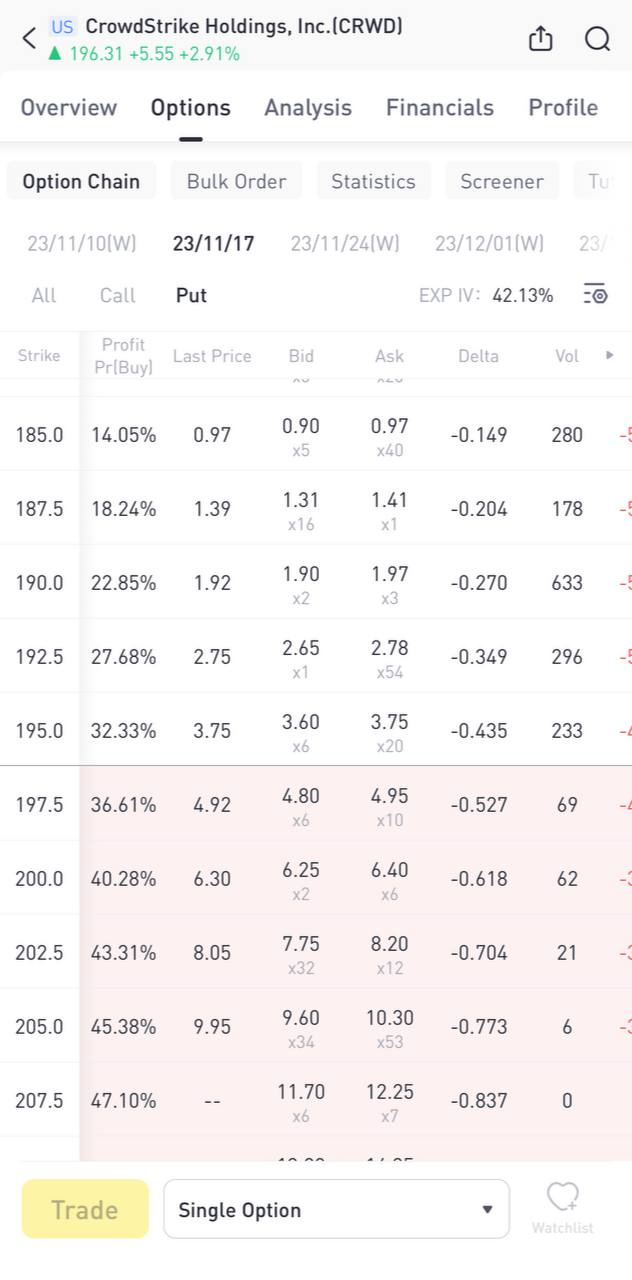

13th November Intended Trade:

Short 3x Crowd Strike Puts for $190 or $192.5

My rule of thumb is to keep credit per share / strike price at about 1% and to stay at about .3 delta. I’m fine with going lower if I feel the share price is not as attractive as I wish it to be.

The goal for that 1% mark is simple, if the shares fall and still trigger the assignment, I have a 1% buffer (minimally) over and above the initial fall from its current share price.

This numbers can shift obviously and is more difficult to share in a post. But the above rule of thumb should help guide your decisions.

Why CrowdStrike?

Crowdstrike is a leader in endpoint security. Put simply, all the devices used by people to tap into the digital world. Phones, routers, laptops, tablets, ipads, and more.

There are 3 simple ongoing trends in our world:

Amount of devices being used per person is going up

Amount of data being user per person is going up

Digital consumption, generation, and participation (entertainment, shopping, leisure, learning) is going up

These 3 simple facts are not standalones - they multiply off one another exponentially.

Today, it is not uncommmon to see the average person with:

A tablet/laptop

A smart phone

A traditional PC

A smartwatch

Smart kitchen/living room accessories

Smart gates, motion sensor activated cameras, etc

The per capita generation and consumption of data has skyrocketed since the 1990s and this means the amount of endpoint vulnerabilities has skyrocketed as well.

This is obviously good for Crowdstrike’s business.

Per Crowdstrike data:

70% of successful data breaches originate at the end point

80% of the most valuable security data collected come from the end point

90% of successful cyberattacks originate at the end point

More then that - the rate of growth that CRWD has maintained is phenomenal and to me represents evidence of several key factors:

The right processes and people are embedded within the system

The right product-market fit

The right timing for that product market fit

A generous amount of demand for that product

A key competitor, Microsoft (a juggernaut in its own right) fares poorly in direct competition: 8/10 times, cusomers choose CRWD over MSFT solutions. Its to be expected since MSFT didn’t come into being as a securtiy focused company like CRWD.

In addition, Crowdstrikes enjoys 3 of the strongest moat characteristics in the business world:

Essentiality - Their business is a small but essential part of any digital based business

Network effects - Threats analysed and detected for one client is now updated to reflet across all of CRWD’s clients.

Switching Costs / Aversion of losses - There are operational risks when it comes to taking down your protective digital walls. Loss of analytics during the changeover, project execution, and operational disruption are all key factors. These are standard factors you will know well if you do any form of project management.

Per Morningstar: “CrowdStrike’s gross retention has remained well above 95%, implying a customer lifetime of more than 20 years. At the same time, by upselling its customers into buying more Falcon modules and agent expansion, CrowdStrike has a net retention rate of more than 120%. We expect increased customer stickiness as the firm continues to expand its client base and set of solutions.”

The implied evidence to me is plenty that there is a long term secular tailwind behind CRWD’s ability to earn good profits on work done and to do so in an exceedingly profitable manner.

Conclusion:

Long CRWD 0.00%↑ by shorting puts. Earn the premiums if the company share prices track upwards. Hold the shares and sell calls at above average prices if assigned. Buy shares over long term dips.