Occidental Petroleum: What Can Investors Get Looking Forwards?

Occidental Petroleum: What Can Investors Get Looking Forwards?

Why is Buffett still buying?

About the Business per Morningstar:

“Occidental is one of the world's largest independent oil and gas producers. Its upstream operations are spread across the U.S., Middle East, and North Africa. It also has a consolidated midstream business, which provides gathering, processing, and transport services to the upstream segment, and it separately holds an equity interest in WES Midstream (a remnant of the 2019 acquisition of Anadarko Petroleum). The portfolio also includes a chemicals business, which produces caustic soda (an industrial alkali) and PVC (a construction material). The latter segment benefits from low energy and ethylene costs and profitability is determined by the strength of the broader economy.

The $57 billion Anadarko deal was a huge undertaking for Oxy, which itself had an enterprise value of about $50 billion at the time. The cash portion was partly financed with a $10 billion preferred equity investment from Berkshire Hathaway along with the proceeds from the sale of Anadarko’s Mozambique assets (which Total purchased for $3.9 billion in late 2019). But these arrangements still left Oxy with a huge debt burden at an inopportune moment, right before the pandemic. To its credit, management was able to steady the ship by severely cutting back on capital spending, selling assets, refinancing short-term maturities, and temporarily suspending its dividend. And the firm took full advantage of the subsequent rebound in commodity prices, generating enough cash to fully repair the balance sheet and pave the way for significant capital returns. The firm is obligated to match distributions above $4 per share annually with preferred equity redemptions.

The midstream segment also includes Oxy Low Carbon Ventures, which partners with third parties to implement carbon capture, storage, and utilization projects. This activity differentiates Oxy from most peers, which merely focus on curtailing their own emissions. Oxy's experience sequestering CO2 for enhanced oil recovery potentially enables it to go further, and management has ambitious plans to develop a network of point-source and direct air capture facilities that should help Oxy get to net zero by 2050, and generate incremental revenue, too.”

Forward Returns

All business are valued on a combination of 3 primary factors:

growth (revenues, operating cash flow, free cash flow)

yield (dividends / share buybacks)

change in multiples valuation (market optimisim / pessimism)

Some secondary factors affect the above 3:

How long can the company survive?

Affects multiple valuation

Affect total yield available to shareholders (longer the co survives, the more dividends it pays out)

What is its reinvestment runway?

Bigger market = triple boost from higher earnings + higher valuation + higher possible yields

How pessimistic is the market on the future returns of the underlying industry?

Shipping for example is a well known capital destructive industry. My aggressive investments from it only benefitted me via EURONAV paying out so much in dividends. The rest of my positions only saw marginal gains despite large increases in earnings. Valuations didn’t change because the market was pessimistic on valuation and my main means of shareholder returns was dividends.

This was an important lesson —> Always look for places where there are 3 possible sources of returns: change in market outlook / valuations, change in earnings,

Occidental Petroleum’s Forward Returns

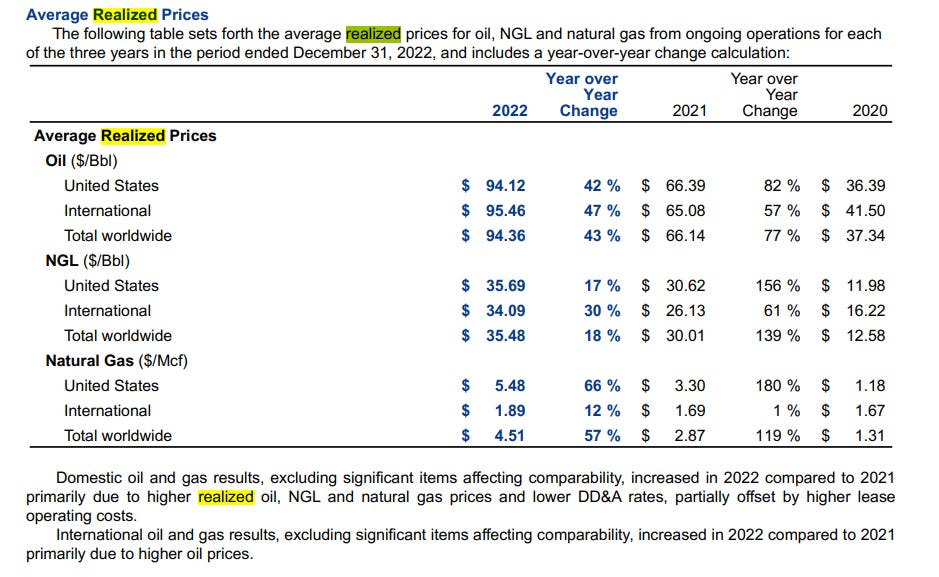

Oil averaged realised $66 in 2021.

Oil averaged reaslised $94 in 2022.

Net free cash flow per financial year 2021 was $7.56 and $12.21B respectively.

For argument’s sake, let’s pretend oil averages $70-80. Free cash flow should come in between $9B and $15B post the crown rock acquisition (if the deal is 25% accretive as expected). If its only 10% accretive, free cash flow will come in between $8.3bn to $13.4bn next year.

Against an approximate enterprise value of $80.79B, OXY currently trades at around 10-16% fcf/ev prices based on $66-$94 oil prices. Current oil prices sit around the 7-handle.

In the worst case scenario, the company’s breakeven price per barrel of oil sits around $40.

While the price of oil can be volatile, if expected returns can average 10-16% per year, it’s not too bad and its worth taking the risk. Between dividends, shareholder returns and debt paybacks, assuming no crazy tail event, investors today can net between 10-25% returns on the next 5 years.

As an upside, the CEO has placed a strong emphasis on fcf generation, share repurchase, and dividends to shareholders. This is expected since Berkshire now owns 28% of the co overall. Managment can be called “aligned” in this case though I’d prefer they smash the buyback button over handing out taxable dividends.

In 2022, OXY returned nearly $3 billion to shareholders through dividends and buybacks alone. That’s 3.7% shareholder returns in a single year alone.

Investors who prefer more stable, high return on capitals business should probably avoid this. But investors who are able to stomach some volatility might find this interesting.