Megaport: Network As a Service is About to Explode

Megaport (ASX:MP1) and how they 28x'd their revenues in 5 short years.

Grasping Secular Tailwinds

One of the first few things I learned when I entered the investment world was to look deeper at the world around you.

Often, what was unforeseen by market pundits could have been seen easily enough if you just identified secular trends and invested behind the few players that truly mattered.

Semiconductors are a key example (trucks and freight rates going ballistic another).

I don’t feel smart very often, but when I do, I like to remind myself how I missed out on the semiconductor stock run ups as the world normalized to IoT/5G whilst I bought myself a computer, considered getting a phone, an iPad, and still had a laptop.

The number of chips/person in the developed world exploded from 1 to maybe 5 and probably in my lifetime, will go to 15 to 20 / person. That’s an exponential leap in the number of chips required. All of which require their own level of updates, increases in power, encryption, data transmission/storage, so own and so forth.

That necessary power jump in capabilities/decrease in size/cost/power consumption necessitated more complex production which invariably led to greater outcomes for chip manufacturers (ASML, TSMC) and its peers (LRCX, AMAT).

Yet the world’s supply chains were never built to provide for an IOT world. We were prepared to chip planes, phones, laptops, and computers but not literally everything else.

We were far less prepared for the supply of these chips to dwindle amidst covid production halts. Buoyed by demand and surging prices, as well as what the markets expected 5g/IOT to look like 10-15 years from now, chip manufacturers, and anything “picks and shovels” related to the manufacture, testing and deployment of semiconductor chips have seen an upswing in share prices.

Is this rally justified?

ASML, the world’s only EUV machine enabling 5nm or less chips (yes, literally, a monopoly) saw revenues jump 33% in a single year.

Yet. despite noticing the uptrend in 2017 (around the time I considered switching back to an iPhone), I still didn’t manage to catch the upswing (approximately a 39% cagr, an approx. 3-4 bagger).

What industrialization (the process of reducing cost of goods/services via aggregation or economies of scale) is affecting today is a far cry of the 1700s. In those days, it was simpler materials. Cotton. Yarn.

A list of some of the things that have gone down in cost thanks to industrialization/globalization:

Food

Travel

International logistics

Brokerage costs

Energy

What’s left?

Megaport’s (ASX:MP1) proposal is the cost of network connections. To explain Megaport’s value proposition, I first have to digress and explain the internet.

How the Internet Works…Sort Of

Put simply, when you’re reading this, its because your computer is communicating with your wifi router via radio waves, which your router then encrypts and transmits to local data centers, where it is cross connected to overseas servers hosted on local servers.

These oversea servers are connected by subsea-cables which connect (yes under the freaking sea) to far away data centers.

This is necessary because any single network connection (your computer, wifi router, optical fibre cable, and local data center count as one network) needs to be connected physically to another server/network for information to be exchanged.

Not being connected can have dangerous results.

“In one famous de-peering episode in 2008, Sprint stopped peering with Cogent for three days. As a result, 3.3% of global Internet addresses ‘partitioned’, meaning they were cut off from the rest of the Internet…Any network that was ‘single-homed’ behind Sprint or Cogent – meaning they relied on the network exclusively to get to the rest of the Internet – was unable to reach any network that was ‘single-homed’ behind the other. Among the better-known ‘captives’ behind Sprint were the US Department of Justice, the Commonwealth of Massachusetts, and Northrop Grumman; behind Cogent were NASA, ING Canada, and the New York court system. Emails between the two camps couldn’t be delivered. Their websites appeared to be unavailable, the connection unable to be established.”

https://www.scuttleblurb.com/ - EQUINIX post

(highly recommended)

Beyond that, dependability, speed, flexibility are all key to the modern economy.

The first five seconds of page-load time have the highest impact on conversion rates.

If an e-commerce site is making $100,000 per day, a 1 second page delay could potentially cost you $2.5 million in lost sales every year. (neil patel: https://neilpatel.com/blog/loading-time/).

The highest ecommerce conversion rates occur on pages with load times between 0-2 seconds.

Website conversion rates drop by an average of 4.42% with each additional second of load time (between seconds 0-5).

The average mobile web page takes 15.3 seconds to load.

Nearly 70% of consumers admit that page speed impacts their willingness to buy from an online retailer.

Of all the people surveyed, half said they’d be willing to give up animation and video for faster load times.

As page load time goes from one second to 10 seconds, the probability of a mobile site visitor bouncing increases 123%. (google, 2017)

As of 2021, the ecommerce industry had an approximate collective value of $4.9 trillion US dollars. Can you imagine the amount of money lost because a page didn’t load fast enough or a server didn’t respond fast enough?

Can you imagine running a fully online web based business with anything less than top-notch, reliable, dependable, always up internet/servers?

I can’t.

Yet the cost of setting up and running such a service can be extremely prohibitive as businesses scale in need and consumption.

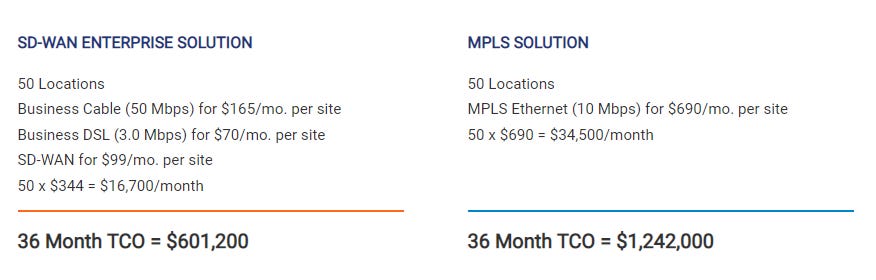

To have that top-notch, reliable, dependable, always up internet/server/connections, firms traditionally turned to what the industry calls a MPLS (multi-protocol label switching) circuit. Without going into technical jargon, it’s basically your own private “network” of connections with guaranteed uptimes, speed, and reliability secured by a service level agreement.

MPLS(s) are reliable and efficient, but expensive, and time consuming to set up with a lead time of anywhere between 1-6 months depending on the area you’re working out of.

The arrival of SDWAN (software defined wide area network), a key piece of Megaport’s network infrastructure offering changes everything.

Utilizing their own connections, Megaport’s proposal is straightforward, instead of dealing with multiple vendors at all the various data centres, instead, connect with megaport - they have already built out connections themselves so you don’t have to. You can piggyback off of their network and set up fast, seamlessly, and with way less costs. The network you want can also be configured to the speed and capacity you want.

Depending on who you ask, and I’ve asked 3-4 different network integrators/engineers, the savings can be upwards of 40% or more compared to MPLS.

When you’re talking millions a year, and hundreds of million by the bigger organizations, that’s a huge cost saving.

Who wouldn’t want some of that?

If you’re intrigued up to here, that’s good. But remember that the internet is physical - not some ephemeral beast that lives only in the atmosphere.

It’s made of a globe-spanning connected maze of fiber cables and subsea cables and more routers and switches than you know what to do with. Hosting servers, connecting cables, ensuring everything runs smoothly takes money - a lot of it.

While it might be inefficient for a small business owner to link up his whole network to a local data center then pay fees to multiple separate vendors to manage multiple separate servers hosting all his connections, Megaport’s bet is that its efficient if you can go big enough.

In other words, this is a scale game.

The larger Megaport’s own sprawling network of connections is, the more businesses can use Megaport’s connections as their own (for a fee of course) and the more efficiently Megaport can leverage businesses off their largely fixed operating costs. In case you’re wondering why Megaport “gets away” with finite operating bandwith and theoretically infinite amounts of demand, remember that network usage is seasonal/event based and not everyone needs to use the network w the same amount of bandwith at the same time.

In the same way that most car owners don’t drive 24/7, Megaport is able to utilise the “spare” hours to turn the “car” into a productive asset. Unlike Uber’s business however, Megaport doesn’t have drivers to pay and infrequent demand. Megaport’s customers spend on the platform and frequently increase their spending.

Profitability however is an issue. Any scale system needs to get large enough, fast enough to be profitable.

As I mentioned earlier, it costs money and time to set up a vast sprawling network of interconnected tubes among data centers. As of now, Megaport is still unprofitable.

In fact, on every identifiable metric, Megaport virtually qualifies as uninvestable. It has negative operating cashflow. Doesn’t make profits. And despite growing quite nicely, still appears to be bleeding massive amounts of money.

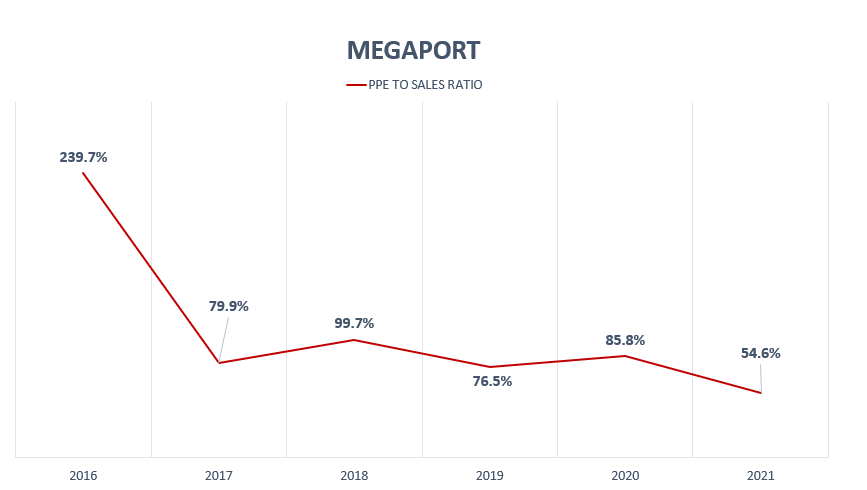

But it is inflecting. PPE as a % of revenues is continuing to dip down. Losses as a % of revenues is continuing to drop. Both are signs that the operating leverage inherent in the system is beginning to work.

With enough time and more than enough cash, Megaport should be able to inflect positively over the next 2-3 years and when that happens, the business should re-rate higher.

Where Does Growth Come From?

As can be seen, Megaport makes money basically from the transmission of data.

There’s more pricings available on their website. But you get the gist of it. More data generated → more data transmitted → more revenues for Megaport. Pair that with a disruptive business model and a huge secular tailwind from IoT and a world where everything is chipped and you can begin to see why I am bullish.

In addition, Megaport’s partners, the largest network vendors in the world VMWare, Fortinet, Cisco Systems now enlarge their ready salesforce by several orders of magnitude. It’s one thing to be on the street selling your own stuff. Its another to have the world’s biggest and best players in the network area help you do it at no cost.

Risks

There are some traditional risks here.

Execution can fall apart.

The company might never scale up fast enough or profitably enough.

The technology might be copied. Megaport is not the only one in the business pursuing this line of thought - there are others.

They might run out of cash and never be able to raise more.

Some kind of futuristic technology might render network connections the physical way invalid.

Look around and throw a stone. You’ll find some kind of risk here no matter what.

Summary

Megaport is a play on the transmission of data exploding to unbelievable levels. I believe their revenues will scale along with that nicely. I also believe that the operating leverage inherent in their business will similarly lead to (a) large increases in revenues, and (b) profits.

As of latest trends, Megaport continues to grow revenues and monthly recurring revenues at a 40%+ clip. Losses continue to shrink. I believe an inflection is coming. And with that inflection, a big re-rate in per share value. That said, this is a barbell sort of idea. Something you put 2-3% in. The risks are too improbable to estimate accurately even though I’m reasonably certain I have the edge in a variety of outcomes.

If I lose, I lose 2%. The company’s size as a percentage of portfolio gradually decreases to nothing.

If I win, and Megaport progresses as I think it does, this might just be a very long term holding that could drive much of my return without more efforts in finding worthy investments.

Disclosure: I am long megaport as of $13/share. This is not to be construed as investment advise. Please do your own due diligence.