Facebook: Why I Bought Then Sold The Position

Facebook: Why I Bought Then Sold The Position

It's been a long time coming

Disclaimer: This is not investment advise. Please do your own due diligence. I currently hold no position but may initiate one at any time.

User behavior and system matters

Trust matters

Feedback loops matter

Facebook is a beast riding a significant and ongoing trend: small business’s need to deploy marketing campaigns that are measurable, modifiable, scalable, and replicable, on areas both niche and mainstream.

Read that again. Because each word in that sentence matters a hell of a lot.

Facebook’s Success: Enabled by Google’s Bell Curve Search Features

Traditional marketing used to be pretty simple. Buy a bunch of ad space on television, radios, and newspapers. Reach out to Oprah or Dr Oz, or the Tonight Show or somebody in mass media and pray/hope to get an interview or pay them to have a slot on their show where you can air your product/business and then hope to drive enough traffic/user awareness so your product grows.

The first paradigm shift came with the internet and specifically, Google, the world’s current number one search engine.

And Google’s an ephemeral beast.

35% of the traffic goes to the first link that’s on the first page of the google search result.

The first page of google receives 95% of the traffic. Less than 5% goes to the second page of the search engine.

SEO algorithms (from what I’ve heard) change frequently and no one can truly guess how good a certain article is and if good, how long it’ll stay good. There’s a limited number of people who can be on the first page of results (bidding wars are expensive for frontline properties too!) and if you’re not on the first page’s top half - good luck getting any traffic if ever. And so legions of marketers have devoted themselves to immense amounts of research and backlinking and content Search Engine Optimization in order to try and be at the very top for the relative “search terms” they think their users might go on Google to search for. The result? Intense amounts of frustration. If content marketing in a competitive niche sounds complicated, that’s because it really is.

Business owners need to be aware of search terms, bounce rates, time on websites, increasing/decreasing readership levels week to week, month to month, topic by topic. They need to craft content that matters. Structure it in a way that Google's Algorithm will find relevant/useful to readers (and vice versa) and then execute: hope that readership leads to product/service awareness that leads to revenue that leads to profits.

The second paradigm shift came with Facebook. What was not apparent immediately to a lot of people at the time was Facebook’s ability to compel crowds of people to connect online and feel more included in everyone else’s lives.

Once Facebook left campuses and went mainstream, the race was pretty much off and all Google could really do was stare at the trail Facebook was blitzing up its garden path, growing 22x from $3.7bn in revs in 2011 to about $85bn as of 2020.

Meanwhile, Google’s managed to grow revenues about 5x from $37bn to $182bn. That’s no measly sum either, but 5x is a quarter of the growth Facebook had.

The questions has to be asked on why Facebook was able to carve significant and growing chunks from what was a supposed “monopoly” end market - online advertisers.

The how and the why matters in this respect.

Facebook is a platform for connections, but also increasingly, for forums and communities and knowledge pools. This creates interactions, engagements, and deeper specific uses. If you’d like, you can think of Facebook as Reddit but…monetized and public versus mostly anonymous.

Let’s take me for an example. I’m a frequent user of Facebook. I’m involved in and lurk in multiple gaming, coding, investing, and physical health routine communities. I counted 8-10 the last time I checked. I don’t always keep track either. When I need specific information, I pop in, hit the search bar, and type out whatever it is that I might be looking for. Let’s say….a strategy in a game for instance and how to not lose to it for the fiftieth time in a row.

Sounds really specific, right? Except if I’ve gone through that pain, I can guarantee the community has had similar experiences and know how to counteract it.

And this can be a recurring thing for anyone and anything. Relationship problems. Gardening. Counselling. How to make lasagna. How to make Briyani. Or Assam Laksa. Or even onsen eggs.

etc cetera.

Facebook’s value to me as a user here is strictly in the form of its higher quality answers. I’m getting replies from people who have cooked, are cooks, or are higher ranked game players, or physical health coaches who don’t mind giving out free advice for the awareness it brings them (and the flood of clients who follow).

Trust and quality, in other words, are the new marketing norms and Facebook has been capitalizing on that for the past decade whilst Google could only really just…twiddle its thumbs and whistle. They weren’t in the same game and they’ve never really been able to do the same thing.

If you think about it, Google is a search platform mostly meant for search/answers/information. And that information relevance/specificity is significantly limited to the first page. As of 2015, something like 95% of most people don’t click to page two of the google search results.

There is a stark contrast therefore in the usability, and usability drives engagement which drives attention which drives advertising needs/marketing dollars.

This user behavior is just one facet of why Facebook is still a superior tool in marketing (pre-Apple’s ios changes, which for now remains unknown, and frankly probably after too). The other side of it is the niche.

All of those things I just mentioned. Cooking. Starcraft 2. Dota. Counter strike. Valorant. Chess. Finance. Investments. Arm routines. Physical flexibility tips. Cooking tips.

All of those interests and areas are niches for advertisers/small businesses looking to answer specific needs.

Full time game coaches and streamers can advertise and push for more viewers/subscribers. Writers can push for newsletters. Fitness coaches can push for 1-on-1 lessons. Cooking class providers. So on and so forth. And Facebook can do this at an incredibly cheap scale because a cook can advertise a class in a country and even break it down to ethnic-specific cuisine (western, thai, indian, chinese, muslim, etc cetera).

Can you say the same for Google?

Sure. Maybe.

But you’re gonna have to be on the first half a page, or you’re gonna have to be searched specifically for by people in order to get there. And to maintain being on top of that position, you got to keep on increasing the usability and relevance of your website in accordance with whatever updates Google’s algorithm might roll out year by year (which by the way, is not revealed to the public beyond general guidelines).

Can you just imagine the frustration of small business owners who now not just have the need to keep up with their business economics and solutions/competitions but also have to keep up with a increasing litany of complex terms and jargons whilst navigating the field of google marketing?

Having put things into perspective for you, are you really surprised Facebook’s dominated its niche growing 22x whilst Google’s barely managed 5x?

Probably not. But this isn’t the end all be all of it. User behavior differences (not skipping past the first page of Google search vs being presented with relevant ads which you help Facebook amend when irrelevant btw, neat eh?) and complexity of running a marketing operations aren’t the only things tilting the wind in Google’s sail whilst pushing it in Facebook’s tail.

There has been a significant and growing trend of small businesses. Call it what you will, but it’s easier now than ever to start a small business of your own. The concept of finding 1,000 true fans who will buy/subscribe to anything you create because they are a lifelong fan of what you stand for/represent/mean to them is more freeing in today’s working environments where the payoffs are substantially higher and where the “work” is really mostly hobbies/passion taken to next level blogging.

Whether it’s substacks, blogs, podcasts, youtube video creators, or twitch/facebook (nudge nudge, see what I did there?) video streamers, OnlyFans adult content or online coding classes (https://codewithmosh.com/), more complete online courses (https://www.udemy.com/) or upskilling based content, there’s just…immense amounts of a growing, fragmenting, self segregating market.

Put into perspective, this favors Facebook’s operating business model immensely and significantly disadvantages Google’s. When you don’t have the content/ability/dollars to get onto Google/Youtube’s first two page of results, without Facebook, you’re doomed to basically word of mouth and to toil away in obscurity.

What else can a business do?

Multiple small business owners I know or have worked with personally can confess that their business wouldn’t be where it was today without Facebook’s immense marketing effects. Take that away and sales can plunge 50-80% over night.

There Is No Alternative.

Because until Facebook arrived, no one else was as adept at allowing people to self segregate their interests and then be presented advertising relevant to their wants and needs versus advertising they find just plain irritating.

Don’t believe me? Then why haven’t millions of people uninstalled Facebook from their phones yet? According to latest numbers, there were 1.84 billion (yes, billion!) daily active users on Facebook as of Dec 2020, an 11% increase!

Anecdotal as it may be, this is at odds with Youtube (where we famously have YouTube ad blockers to enjoy our videos in peace and quiet).

I’ve been hit with consistently irrelevant and irritating ads on YouTube (mobile games, investment course offerings) whilst on Facebook, I’ve mostly either stopped to take a closer look or just clicked through entirely.

Ditto for Google.

When I search something, anything really, it’s almost ingrained behavior for me to move on from the first 4-5 “presented” results because most of it are ads and….I’ve learned most of them aren’t what I want unless I did a specific search.

And I’m not the only one. If I was, Facebook’s return on investment for marketers I know wouldn’t be so damned high compared to Google AdWords or SEO rankings. And a high return on advertising dollars plus a limited budget plus a large volume increase in content/service/product providers will mean an almost concomitantly large increase in need for advertising.

Put another way, Facebook is going to keep eating up Google’s share of the business. But the two titans are basically oligopolies in the advertising industry. So it’s kind of hard to say that even with the industry evenly split, Google is on the bad end of things.

What Matters: Trust

Trust is an incredibly powerful tool and a feedback loop that Facebook has which Google does not. Or to be more precise….which Google does not explicitly enjoy.

Google’s “trust” factor is embedded in its algorithms. The more hits and relevant the page is, the higher it is ranked. The more users stay after landing, the higher your page ranks. If people keep returning, the higher you get ranked.

Relevance is everything, and trust is formed on that relevance.

Facebook’s trust factor is in the recommendations friends make to one another on its platform. What book to read next, which show to look at next, where to eat for our next meet up, which movies were good, what cafes were nice…

Word of mouth and recommendations have always been the preferred marketing tools of great companies for a good reason.

They’re free, spread like wildfire, and require no effort to maintain - perfect for small businesses to focus on customer satisfaction and wowing clients versus investing in lots of upfront marketing expenses and praying most of it comes back in the form of leads/sales.

What does this mean for Google vs Facebook advertising wars? From a thematic and mechanical (mechanics of the two platforms) standpoint, I think this puts Facebook ahead in the ad wars for trust via word of mouth.

But I also think Google’s ownership of YouTube is what keeps it in the game.

MKBHD is a successful example of what it means to be an online content creator with a huge following (14.2m subscribers) who leads by a “trust” factor.

His honesty, reviews, and criticism of products is about the only reason I even bothered staying to watch his other videos when I’m normally a guy who doesn’t bother watching recommendations. What I prefer to do is trawl through reddit threads and Facebook comments/recommendations in communities before buying a product.

Notice that weird little interaction? Communities are everything.

YouTube has the beginnings of one and it’s playing in a different dimension where creators can only interact with viewers after the content has been created whereas a forum/thread(twitter)/community can keep going and a lurker/participating reader can reap great amounts of knowledge watching the back and forth (twitter enjoys similar user behaviours).

Can YouTube eventually monetize? I think so. It’s started allowing streaming on its platform and live interactions. So I think they’re definitely on to it. Or at least their behavior displays that. There’s still a lot to be said about static information being found when dug up versus having to dig through a video though, so for what its worth, I’d much rather be Facebook than YouTube in the “relevant recommendation based on trust” argument.

But can it do the same thing Facebook can?

I doubt it.

Where Youtube can’t easily (they can definitely do it over time…but it will be difficult to replicate a network effect) do what Facebook can, Facebook can probably do what Youtube does - Facebook already allows video uploads.

Sure, a majority of it isn’t reviews, recommendations, walkthroughs or more full length videos, but who says Facebook can’t slowly edge its way in over time and swallow YouTube’s video market share? Youtube has almost 5 billion video views everyday being watched but Facebook’s grown it through July 50% and is already at 1 billion video views per day. No. Seriously.

Tell me again why you think Youtube’s “moat” as a platform can’t be breached and I’ll tell you to look at Facebook and re-think your stance.

If an up and coming platform previously into the written form and written content suddenly starts massively growing video views and uploads, why does Youtube enjoy a moat that Facebook does not?

And there’s no reason why eventually content creators wouldn’t want to share their videos across multiple platforms for multiplicative reach.

Greater reach, greater ad served, greater revenue for creators means greater margins for FB and the feedback loop continues.

Research And Development: Diworsification or Reinvestment in an Excellent Business?

An excellent business to my mind has only two real traits:

High returns on capital

Large opportunities for reinvestment at high incremental rates of return on capital

Does Facebook really achieve this standard of excellence?

I don’t know.

But we are in the business of guessing and getting it right guessing with a standard of error. As long as we’re approximately right, I think we’re going to be ok.

So let’s take a look at what the management team is going to focus on over the next couple of years at FB.

Some pointers from the latest transcript available freely here:

more than 1 billion people visit Marketplace each month

Shops was launched in 2020: more than 1 million monthly active Shops, more than 250 million monthly Shop visitiors

WhatsApp Catalog is now online, allowing businesses to update and include what's in stock (becoming a more unified online shopping ecosystem) and Carts was also launched on whatsapp last year, and more than 5 million orders have been sent

total daily conversations between people and businesses on messenger and Instagram grew more than 40%.

more than 3 million advertisers are using click-to-message ads

more than 1 million advertisers are using Click-to-Whatsapp ads too

the focus of Zuckerberg on enabling jobs you enjoy versus jobs you don't is in line with the inclination of the economy over time: it gels with people versus moving against people's wishes as the old economy did (university, job, etc)

Live Audio Rooms

Soundbites

Partnering with Spotify to launch music player in FaceBook App

Monetisation as the end goal

There’s a big underlying theme here I think Mark Zuckerberg is trying (and correctly in my opinion) to tackle.

(A) Above, I already mentioned the niche and currently exploding content creator trend. We’re in stage two of the internet phase imo, where the potentials of the web are now not just used for information dissemination but also properly as a means of livelihood whereas before it was only available to companies.

That means more and more people are beginning to realize having someone else in charge of your pay check is increasingly a liability instead of an asset.

Having someone else cut you a check worked in the past because starting and succeeding at a business carried enormous risk. Millions of dollars in hardware and rentals and leases and manpower could eat up capital fast.

Now, you tap a few buttons, get a web designer, sign up with stripe/Shopify/shops, get a Facebook ad agency/book and you have your own marketing/online platform/payment system ready to go - if you have some sort of passion/expertise to monetize of course.

To be fair, I’m not rehashing anything people reading this shouldn’t already be aware of, but I AM saying that Covid did pull forward the timeline and make everyone realize that the industry is changing and changing fast. Facebook recognizes this and is racing to keep up and try to get ahead whilst everyone else seems to be….not really doing anything about it.

Amazon isn’t trying to do it. Google isn’t trying to do it. Twitter is under monetized. OnlyFans won’t work unless you’re into doing porn, and Spotify can’t get into Shops/Video the same way Facebook is.

Is there a guarantee Facebook succeeds?

I don’t know. But the numbers seem to indicate that Facebook is gaining more traction and more users, and that maybe time spent on your feed isn’t as important to Facebook as it was versus time spent browsing/watching videos/streams/Live Spaces, etc cetera.

Valuation Thought Process

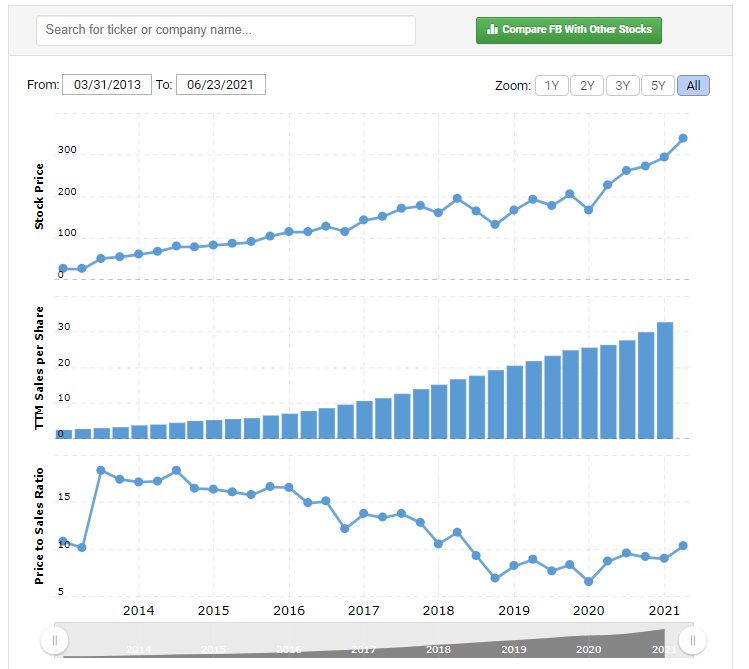

The whole process of valuation is a little murky nowadays so I’ve tried to do it the common sense way. Since Facebook breaks out user data and ARPU on it’s platform, it’s a little easier to do a rough back of the envelope calculation.

Let’s start with WhatsApp. There’s technically no data but we can try to make an educated guess.

There are other messaging apps out there (Telegram, Line, etc) that don’t require monthly payments so I don’t think Facebook can ask for a monthly price and not see a large exodus.

Let’s presume instead that Facebook can start selling ads on WhatsApp itself on a not so intrusive manner and let’s pretend that each user on WhatsApp is worth 1/4 to 1/5 of what each user on Facebook represents.

How much can we value the platform at?

As of 2020, Facebook’s average revenue per user was about $32USD.

At 1/5th the value, with 2 billion WhatsApp users, we can call the annual revenue at about $12.8 billion dollars of revenue before even talking about business subscriptions/other advertising.

Even at 1/10th the ARPU of Facebook’s main platform, we’re talking about $6.4 billion yearly revenues. Not too bad for a $19 billion purchase if true because that’s 33%+/- returns within a year before sorting out capex and reinvestments.

Now what’s Instagram worth?

Facebook doesn’t break out the numbers but some people are willing to talk anonymously. In 2019, unnamed sources stated the app brought in $20 billion in sales (advertising).

If true, considering there’s about 1 billion users, each user is worth about $20.

Can we peg the same value for WhatsApp?

Probably not.

But base case, you’re probably willing to shell out 5x earnings for a private business. Call it $100bn for a $20bn a year business with low capital reinvestments (All platforms from WA to FB probably require an army of developers and techs, but still way less versus say…a manufacturing plant).

Facebook sales in 2019 ex-Instagram was about $50 billion. 2020 revenues accounting for no growth from Instagram segment was about $65 billion.

To sum;

WhatsApp: $6.4bn / year

Instagram: $20bn / year

Facebook: $65 bn / year

So per year revenues can shake out to be about $91.4 bn. At 5x sales, that’s $457bn and at 10x sales, that’s $914bn. Facebook’s enterprise value as of current is about $909 billion.

Where does this leave us? Probably somewhere along the same lines as what everyone else is thinking.

Remember, this does bake in Whatsapp earning a sum of money we haven’t seen or confirmed and this also does bake in Instagram not increasing or decreasing its earnings power with all time highs of $65 billion revenues from the main platform.

This is the steady state case scenario of what the valuation is baking in - which implies “fair” value. Though I’d say that owning a high free cash flow generating business (north of 40%!!) at 10.8x sales is still abnormally cheap.

But….this is the steady state case. Not the bear/bull case.

Our goal isn’t to get a steady state case but to take a look at what can and possibly will happen and aim to buy at a level which is intrinsically and optically cheap given a wide range of scenarios.

So what’s the bear case?

Let’s assume the worst.

User churn off and stop using Facebook as much.

Streamers and other network effect dependencies start rotting off as users stop coming online.

Revenues/advertising starts failing and as that happens, less advertising comes aboard and heads to other platforms (which btw…I’m still waiting on an alternative of).

What happens then? IF the platform does begin unraveling, I think it’ll happen slowly, then blow out all at once. We can assume earnings will be relatively constant until signs of network degradation start showing: declining user numbers, declining user time spent on platforms, declining user statistics overall (probably why FB is so desperate to own the next AR/VR platform).

We know that FB currently trades at about 42x 2020 ending free cash flow so basically anyone who believes that its network will start deteriorating can’t start investing now and expect a healthy return over time on investment. In all likelihood, if the network degradation starts now and becomes terminal by year 6/7, no amount of torturous DCF calculation is needed to tell you that you’re not getting your money back. In addition, network effect businesses don’t go silently into the night like melting ice cubes such as newspapers or radios. They bang and bustle about, trying as hard as they can to restart growth engines and perpetuate forward momentum for the network so they can return to healthy status. That means cash spending and investments and likely means no free cash flow.

So bear case wise, we’re fucked. There’s no scenario we win in a bearish world where FB network deteriorates and we somehow recover some of our money back at 42x 2020E fcf.

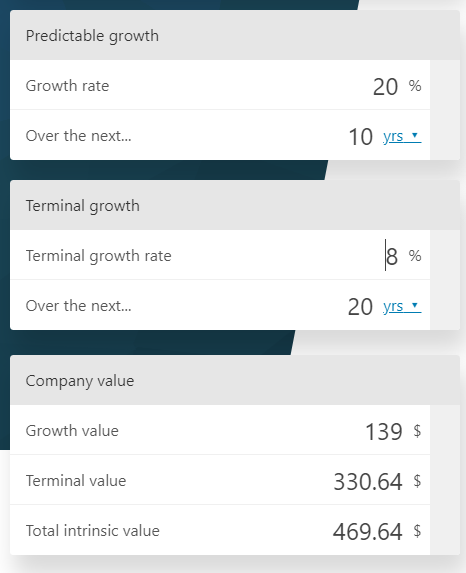

But what’s the upside?

Well. Let’s presume Free Cash flow is the true driver of Facebook’s business value (as it should be imo) and that it can grow as it has historically (22%). I jacked the numbers into an online calculator and here’s what we get.

Of course, there are assumptions. Hazardous ones.

This assumes Facebook can grow free cash flow 20% running for another 10 years.

This assumes Facebook’s terminal growth rate is at 8% and now lower. And it lasts 20 years.

This assumes that the reinvestment rate of the firm doesn’t increase as it tries to edge into Oculus hardware mass production - which is very difficult to do.

This assumes that the growth drivers for FB, the content creator’s economy and the infrastructure it’s trying to build up, will pay off - which is very difficult to ascertain for certain.

This assumes that Facebook’s anti-trust worries are all over, and that no amount of regulation will be coming its way. Again, an extremely tough ask.

But wait.

This isn’t the end of the story.

Shops is a direct competitor of Shopify. And streaming/videos is a direct competitor of Youtube/Twitch, arguably the more well known streaming platform.

What are Shop users worth?

As of 2021Q1, Shopify brought in about $320.7m (q1 transcript here). As of last known reports I could find, they have between 820,000 to 1m+ merchants. Assuming the higher merchant number to bring down the average revenue per user, each Shopify merchant is worth between $2-300.

But simply assuming that Facebook can make each Shop on it’s Market place a Subcription business like Shopify isn’t…realistic. Shop’s been in the game for a while now and has a head start. We have more than 1 million active “shops” on the marketplace. Even if we assume each “Shop” is worth only $30, that’s $30 million that we can add to the baseline ($30 based on 1/10th the value of a Shopify Subscription and also a close approximation to ARPU of Facebook main platform, could be worth more or less**).

What about video?

YouTube generated 19.77 billion revenue as of 2020. Recall earlier that video views were about 1/5th that of Youtube’s. Can we approximate a value based on that? Very loosely. (A) The videos are on FB main platform and this is double counting, (B) Facebook doesn’t charge anyone for ads for its videos….yet. But let’s assume for the sake of FB bulls that Facebook can create a platform where users share videos and similar monetization can happen over time. What’s FB video views worth? 1/10th the value of Youtube? 1/100th? At 1/10th, that’s $1.97 billion USD annually. At 1/100th, that’s about $197 million.

What about streaming?

Twitch generated between 1.5-2bn dollars of revenue from 2018-2020. Both platforms are nearly identical and I find it hard to believe that when monetization arrives Facebook can’t deliver a similar product at a similar rate. Let’s call it $1bn for now.

To sum;

Shop, $30 million - $300 million range

Video Views, $197 million - $1.97 billion range

Streaming, twitch/games/donations/subscriptions, $500 million - $1 billion range

Base case, we can throw on between $707 million - $3.27 billion of value (without or with synergies in between for advertising) per year onto Facebook’s platform if we want to give it the benefit of the doubt for the future.

We derived earlier per year revenue to be about $91.4bn. Even at the higher end, and even with the belief that it’s potential future monetization takes place well, this three nascent features of Facebook barely move the needle, taking yearly revs to $94.6bn. 10x that and you’re paying $946bn enterprise value against FB’s current enterprise value of $956bn.

That’s assuming for, and asking for a lot.

There’s just way too many assumptions to be made here to feel comfortable.

Any upward revision in value that I can see here has to come from multiples expansion or one of its nascent features doing extremely well in a really big way (or even more growth . Say going from 10x sales to 20x sales. SHOP trades at 54x price to sales but it’s a subscription business. So I guess the base scenario is can Facebook get off the ground and go from revenue by ads to platform as a service and force the market to re-rate its PS ratio upwards. Is this a bet worth finding out?

I don’t know. Shopify’s every DNA strand is focused on being Shopify. Couche' Tard’s every DNA strand is focused on cost reduction, merging, acquiring, and streamlining distribution/price. Can we say the same for FB? It’s a hard ask. Certainly, it’s current (10-11x) Price to Sales is at the cheaper end of where it’s been (15-17x).

If we believe that the long term average of FB is supposed to be between 15-20x price to sales, FB is indeed massively undervalued. If you believe Mark Zuckerberg can get the subscription businesses off the ground, then FB may even be re-rated to 50x P/S.

But I’m wary of approaching any investment from a re-rating catalyst standpoint. As Jim Roumell from Roumell asset management likes to say, I like looking for multiple ways to “win”.

Tetra Technologies was one such example (refer to my earlier posts). Antero Resources was another such example. Prices were too depressed and we had hit rock bottom in natural gas prices.

I don’t see multiple ways to win here. I don’t like a dependency on re-rating of Price to Sales. I don’t like having to make tons of assumptions and tons of guesses. Too many moving parts. Too many unknowns. Too much political risk too.

If our job is to give up some portion of cash today for future cash flow streams, durability, and growth, of said cash flows are of extreme importance. If you cannot assess durability, you cannot hope to assess growth well - that turns your “investment” into a “bet”.

It’s why whilst I can stomach the current p/s ratio and bought a chunk, I later sold it, adding it to Couche-Tard instead (now more then 20% of my holdings).

Some obvious caveats. I can obviously be very wrong. But my thoughts are simply considerations you can keep in mind for your own investment.

Cavear Emptor.