Enterprise Product Partners: Underappreciated Infrastructural Moat

The world isn't going to turn without oil for at least the next decade - whether we like it or not.

Short note: I’m migrating the blog to substack.

The UI is just better, and eventually (in 5 years or less), when I have the goal of monetizing the blog - depending of course, on my performance - it’ll be easier to do so.

Recent Investment Methodology Updates

Second, I’ve added some questions to ask myself (which I humbly implore you to ask of yourself as well) whenever I think a company presents a compelling opportunity.

Is the company likely to be worth more or less in 5 years?

You found a compelling idea - what do you see about it that the market does not?

Is time an enemy or ally of the business? And if time is an enemy, is the valuation of the company sufficiently cheap enough to reward the substantial time decay risk you’re taking on?

If you can’t tell whether or not time is an enemy or friend of the company, assume time is an enemy. Further, does the company have offer you, as the investor, multiple ways to “win”? Are there multiple macroeconomic trends ongoing (suburban displacement, lower forward interest rates, debt re-financing at better rates, more/less travelling, greater/lower financially educated populace, capital overflow/starvation, deconsolidation/spinoff/special situations) that will serve to benefit the company, and by proxy, you?

If the company has retained earnings over the past decade, how has it fared on its reinvested earnings? (if the company alternatively, paid a dividend, how has it fared on advancing it’s prospects, growing revenues, free cashflows?)

Always pay less when you can. If possible, get it free (more on this in my next post).

I’ll leave you to ponder on the above question over your future investments. Personally, forcing myself to run through this checklist has eliminated a great portion of the companies I’ve taken interest (such as trucking). Its also helped me realize that I’d much rather “miss out” on the prospective gains these “compelling” companies offer after.

I consider myself to have net-gained investing acumen and experience if I make right decisions consistently and yet have not been rewarded, versus consistently made wrong decisions, and yet have been rewarded handsomely.

Let’s dive in.

Enterprise Product Partners (from hereon referred to as $EPD)

Those of you who follow me on twitter already know I’ve been looking into $EPD Enterprise Product Partners for awhile. Part of the reason is that I’ve always been interested in the energy space.

I like investing in something mankind will need for the foreseeable future short of rapid leaps upward in energy efficiency technology - it’s not a big leap of logic.

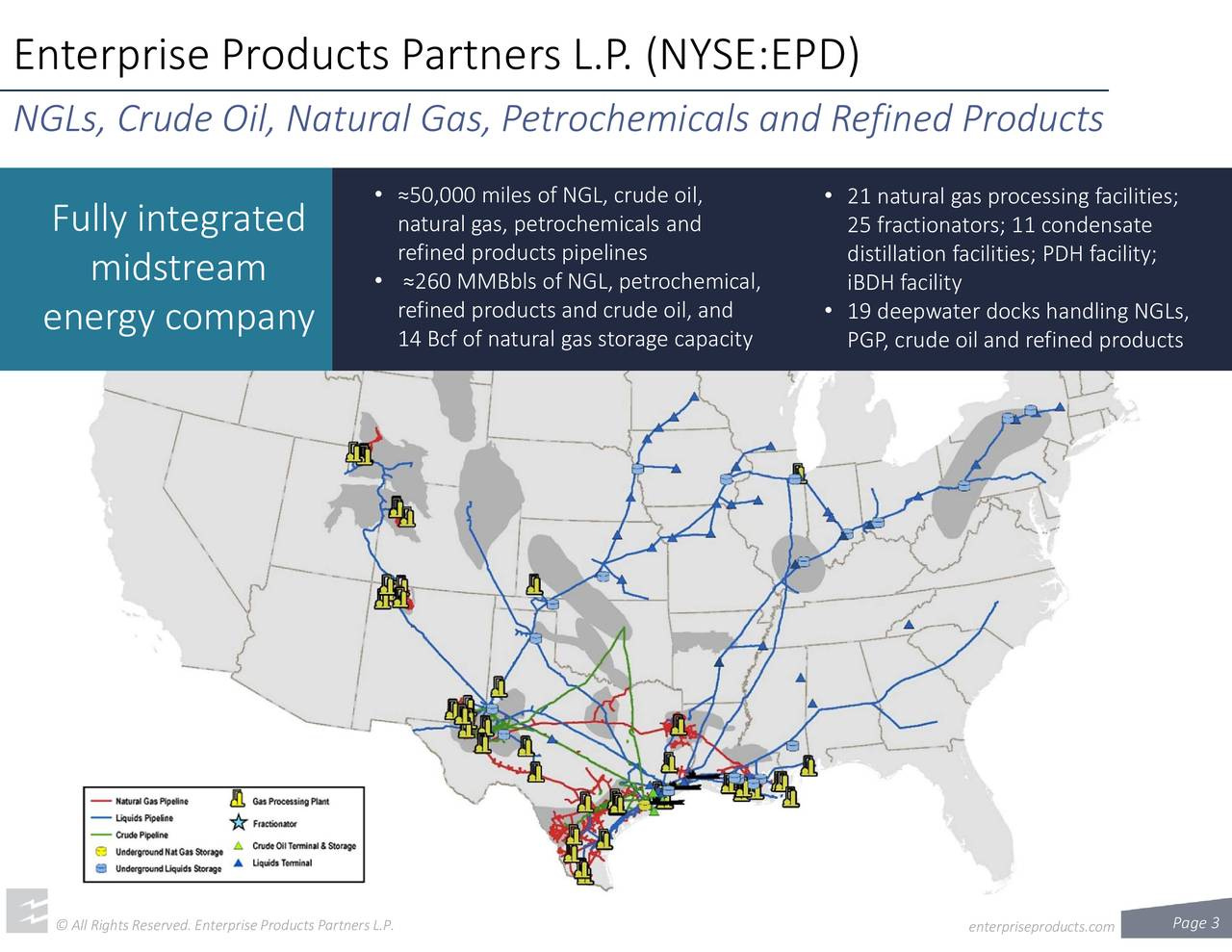

First, an overview. I’ve pieced together the various pieces I felt adequately described EPD’s business so you can paint a better picture.

From Fool.com -

“Enterprise Products Partners has a diversified footprint and an integrated asset base. Its midstream portfolio consists of natural gas, NGLs, oil, petrochemicals, and refined products pipelines, as well as storage facilities, processing plants, and export terminals. Because of its diversification and integration, a given energy molecule will typically pass through five to seven of its assets en route to an end user, and Enterprise collects a fee for each one.

The company is particularly dominant in the NGL infrastructure segment. In 2018, it generated half of its earnings from services tied to those commodities, and hauled in another 13% of its profits from petrochemical-related activities, which typically consume NGLs.

The broader industry needs to invest more than $50 billion on new NGL-related infrastructure through 2035, and that demand will provide Enterprise with plenty of growth opportunities. Add that to its diversification, and this MLP should be able to continue increasing its cash flow and high-yielding distributions for many years to come.”

From Morningstar

”The firm has built out a dominant position in natural gas liquids. Its Houston Ship Channel (where Enterprise has invested over $8 billion in the past few years) and Beaumont Terminal and its Mont Belvieu assets (NGL fractionation, storage, pipelines) means it will be the primary beneficiary as U.S. NGL exports increase in the coming years.

We view the forthcoming NGL demand-pull toward the Gulf Coast as the key growth driver for Enterprise. From its vast NGL system, Enterprise's connection with every ethylene cracker on the Gulf Coast, its sold-out PDH splitter (and its second PDH plant is on the way), and the upgraded isobutylene unit make it adept at converting low-cost NGLs into higher value-added olefins.”

From $EPD’s investor Presentation:

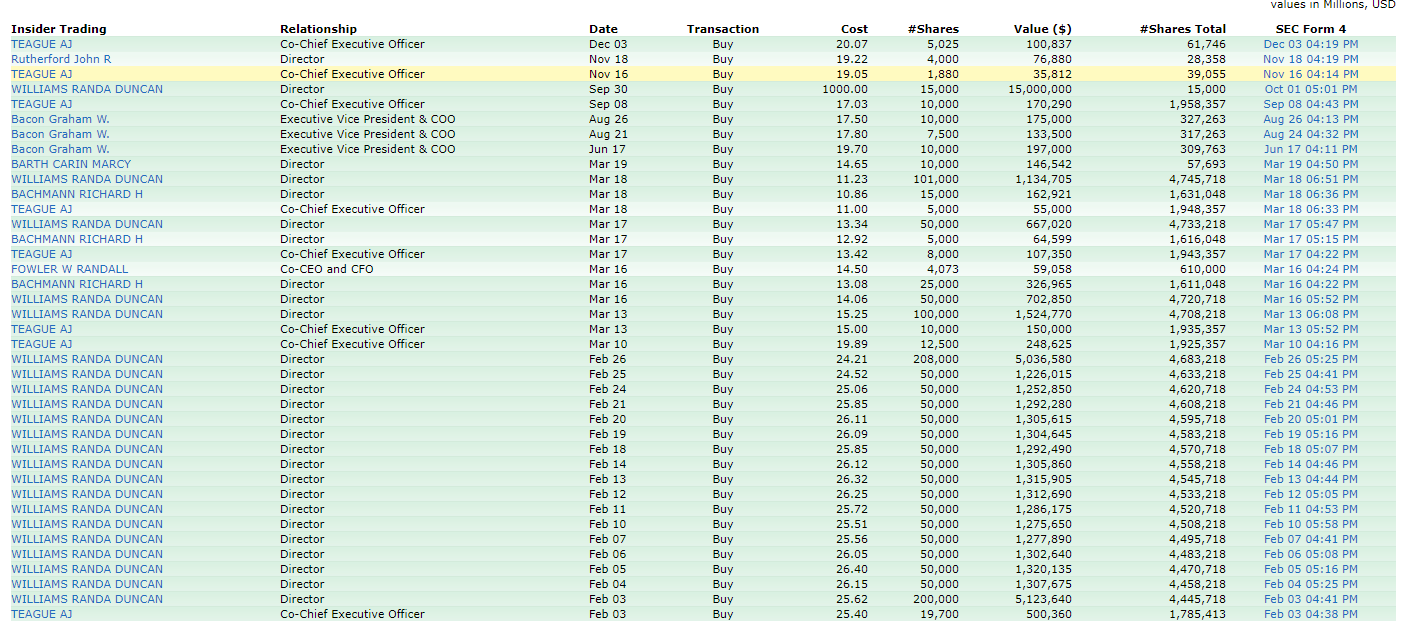

Insider Buying (management alignment, or at the very least, management bullishness)

For those of you who skipped on the images and digesting the information, tldr; EPD is one the biggest, most well-integrated midstream asset in the USA.

In the tech sector, facebook, google, amazon and other internet type companies are the beneficiaries of capex invested by the early telecoms.

In the same manner, I asked myself one fine noon, someone, somewhere, had to be profiting from all that money being poured into the ground for oil/gas - since most producers seem to actually be pretty shit at profitability despite producing tons of what we need.

In my mind, one of two things could happen. (A) We find someone somewhere in the industry that is able to harvest all of the profits from the capital expenditures of others. (B) An industry w no moat has had all its potential advantage competed away and its goods (like the computer, the phone, airplane travel) have become commoditized and we should stay away.

If no one was profiting, then, like the car, the airline, and the computer industry, profits were relegated to the few companies that mattered, and benefits were accrued to consumers: lower price airline tickets, lower priced cars, lower priced energy needs.

Alas, midstream seems to be where most of the profits end up. Even among MLPs however were death traps. Some were captive partnerships(like Antero Resources and Antero Midstream, where Midstream is owned in part by Resources and where Resources is the sole customer of Antero Midstream, hence, the collapse of Antero Resources would spell doom for Antero Midstream) and it took more digging before I found EPD and its peers (Enbridge, Magellan Midstream), most of whom were large enough that they were not held captive to any one producer.

This is where I ‘struck oil’, puns intended.

EPD’s Economic Moat

Many like to call a “moat” a subjective thing. But the truest evidence of any business’s competitive advantage is its ability to earn returns on capital above that of its peers.

Read my lips.

All economic moats conferring “advantages” which most authors wax on about must at some point be shown in the above average returns on capital when compared against industry peers!!

It boggles my mind often when I read reports where authors talk non-stop about a company’s significant competitive advantage but fail to mention the company is barely making any money.

Not All Moats Are Built Equal

Does Amazon have a moat? What about Facebook?

Arguably, both do. But some moats, like the Rubicon can be crossed, at which there is not a point of return.

An example.

A company I was checking out called Old Dominion Freight Line (LTL truck carrier) enjoys significant returns on capital and have done so for years.

Yet, since 2014, Amazon has spent nearly $40 billion (and probably above by now!) on building out and increasingly dense network of logistics and transport hubs. For reference, ODFL’s market cap is a mere $22 billion (although, if u dig into the land they own and you’re able to get a full list of all properties owned, not listed, I think you’ll be able to see that their value is vastly understated)

There’s no moat in the trucking business.

You need a truck. A driver w a license. And fulfillment.

Most people set out to get the trucks and drivers first and the business later.

Bezo’s brilliance was that he got the demand first and then he’s building out the supply.

I highlight competitive advantages and the difficulty in penetrating defenses because companies like Amazon paired with a strategist like Bezos and backed by superb cashflows results in gigantic corporations that can rapidly invade previously “moaty” businesses.

Will ODFL hold out 5 years? 10 years? 20? I’m not sure. But I’m certain that Amazon can replicate its strategy to own greater and bigger parcels of land - especially when the company is incentivized to do so. I’d need to be an industrial land specialist to be able to check whether ODFL has the ability to carve out a small local pie for itself where Amazon can’t ever invade, but that involves far too many variables and has far too many consequences if I’m wrong.

The midstream asset business is a whole other ball game.

Unlike the trucking business or the airlines business, with virtually no competitive advantages and where someone like Amazon can muscle in with unlimited free cash flows, the oil pipeline business is a regulated, need only, exhaustive, and painful process that can take up to 3 years and plenty of reviewing committees, permit approvals, and regulatory requirements before you get approval.

More;

Scale matters with pipelines. Its common sense. You don’t need a business degree (i’d argue attaining a business degree doesn’t seem to contribute much to common sense points among those I’ve engaged with often) to figure out that the more pipelines you have connected to dense areas of production and usage, the cheaper your services tend to be because of the reach you have, and the more business you’ll get.

Cost efficiencies matter. Why? You have access to greater materials since you can guarantee volume as compared to the guy building out one single pipeline, who’ll have to acquire materials at base cost with no discount. Business 101 still applies here. Smaller competitors, even with the cash to do it, will be fighting on an uneven level.

Bigger players win…as usual - This is compounded when you consider the fact that if the biggest players already fulfill the need (for example to shift oil/gas from producer to end user), why would the authorities allow more pipes given it costs them votes? Because while everybody likes to live in a 1st world country, nobody wants an oil pipeline in their backyard.

I mentioned previously that connections to dense production/end users matter. EPD has that in spades. It’s connected to major onshore production basins (Permian, Haynesville, Eagleford, DJ, Green River, Piceance), and throught its shipping networks, refineries, and cracker plants, plus storage, transports, refines, ships and pipes this liquids to end users in the industrial markets/residential markets - it’s little wonder they’ve been consistently profitable no matter what year you look. Infrastructure is a moat. Infrastructure Amazon can’t build is definitely a big moat.

One of the things I tend to do with any idea is to watch for very long term economic trends which can positively or negatively impact an idea. Im sure kodak seemed like a value stock at one point before value investors wised up to the fact that it was toast. EPD ticks most boxes, it’s exposed positively to inflationary pressures (when the world starts back up again post covid, which will almost certainly send fuel prices up vs today), exposed positively to higher or even baseline energy demands, exposed to greater future natural gas exports and in general, has no real downside. The greatest risk i can think of is extreme, sustained, lower gas demand and or lower commodity prices. The first indicates a world ending event (most likely, in which stocks will not be my main priority) and the second precipitates a commodity super-cycle, for which I will be comfortable holding pipelines.

At 8% yields, a lower than industry debt burden, with multiple ways to win across various macroeconomic situations, I just don’t think this is a hard choice to make.

Long $EPD.