Chipotle: Excellent Business but Overpriced

Ticker: $CMG

Listed: NYSE

Return on Capital 5YAverage: 9.2%

Free Cash Flow per share growth 10Y CAGR: 13.61%

Revenue Growth 10Y: 13.95%

Operating Cash Flow Growth 10Y CAGR: 12.05%

FCF Yield: 1.93%

Target Price to Buy: $740

Current Margin of Safety Based on FCF: -99%

*I’ll explain my thought process behind some of the numbers later.

Business Overview

Chipotle should be a business most of you have no trouble understanding. Some of you might even have eaten its food on a regular basis if you are a US citizen or if you’ve been to the United States.

It’s business model is simple.

Make good Mexican food and sell it for as much as they can afford to. They even have specialized meals.

Cute. But at its core, still pretty straightforward → sell Mexican food for as much as you can afford to.

Financial Highlights

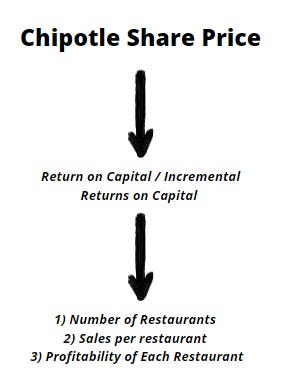

The restaurant business is a simple one to understand. Drivers of the business’s success can be reduced down to;

number of restaurants

average revenue per restaurant

cash on cash returns per restaurant

All three metrics for $CMG are stunning.

Here’s the number of restaurants they’ve operated historically.

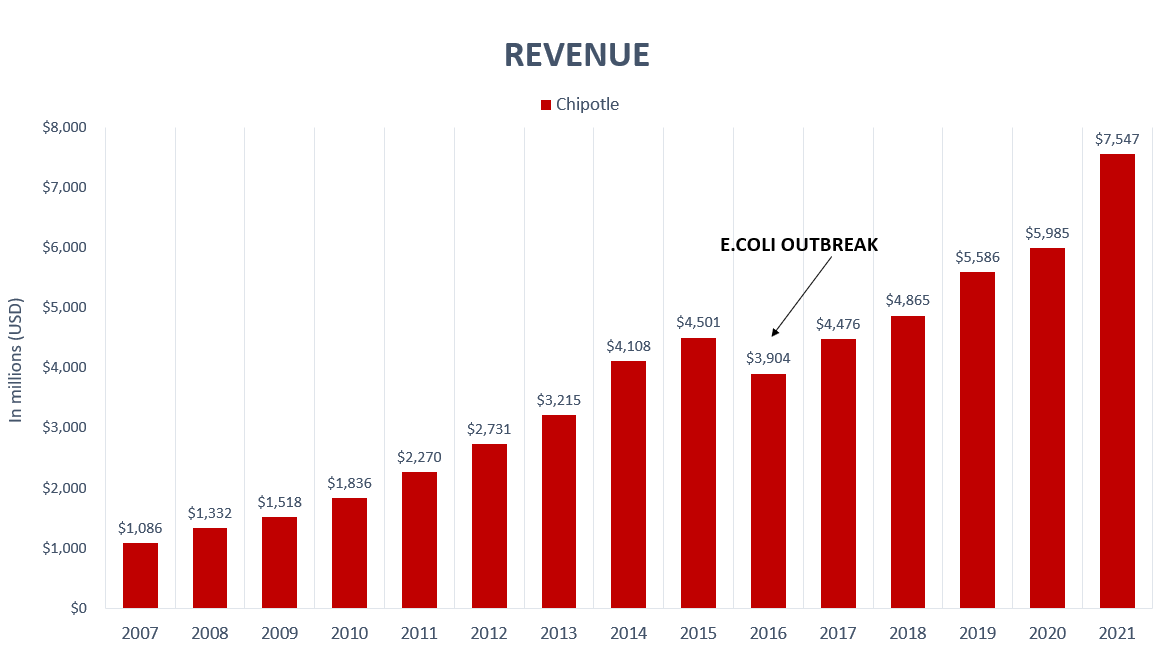

That’s right. Chipotle started off with a mere 489 restaurants in 2005 and have steadily grown its count to nearly 3,000. Revenues have gone along for the ride.

Pretty, ain’t it?

The statistic here is stunning; when a restaurant business is expanding, its very common to see revenue per restaurant actually dip briefly as new openings take time to ramp up to full capacity.

Not Chipotle. Per restaurant revenues has increased about 98% since 2005 despite restaurant count increasing 5x. This cannot simply be luck.

Revenue per restaurants (RPR) has climbed steadily and is now past pre-E.Coli outbreak levels → even with the pandemic raging on in 2020/21/22. Net income levels and margins have also went gangbusters.

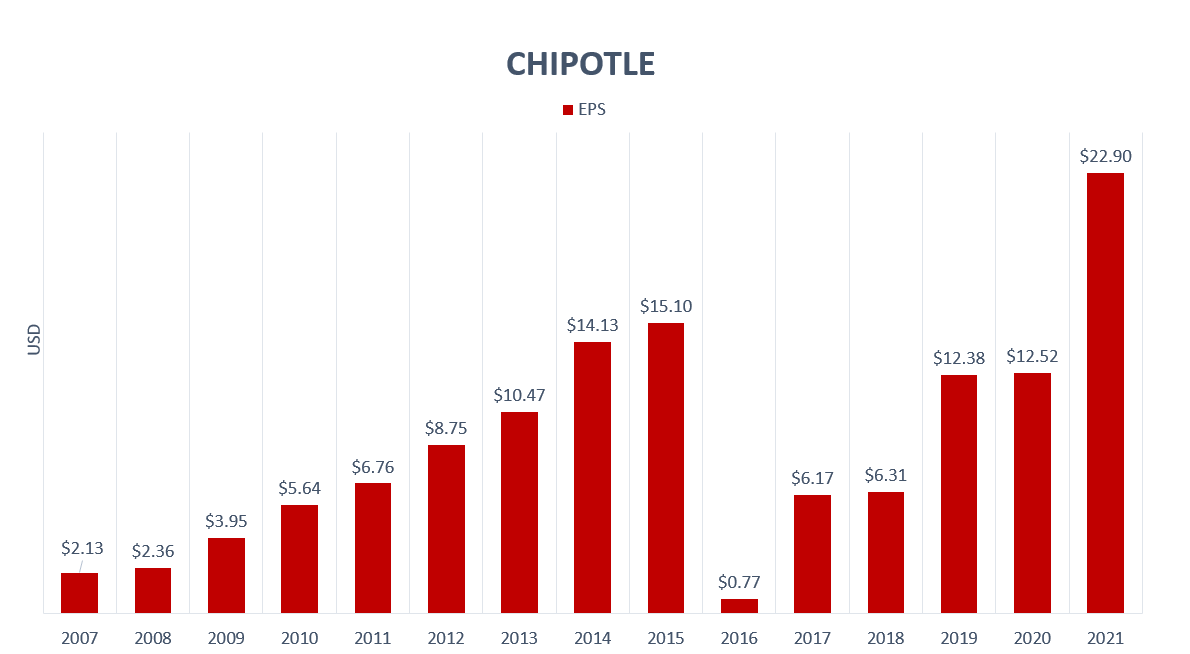

And with it, earnings per share levels as well.

What Drives Chipotle’s Profitability?

At the core, it’s Chipotle’s brand.

This shows up in dominating fashion when we look at food ordered.

It’s a pity I don’t have numbers for 20-22’, but judging by the levels of rising revenues along with Chipotle reporting their own increased digital sales, I’d expect the market share to have expanded or at least stayed the same.

Two Year Payback Period Or Less on New Restaurants.

The return on a newly built restaurant is everything.

On average, it takes between 3-5 years for a restaurant to pay off it’s initial investment. That’s about 15-20% return on investments.

According to management, Chipotle is currently averaging 50% returns on new restaurants. That’s how strong the brand is.

Is management full of shit?

Well, let’s see.

According to Chipotle’s annual reports, as of 2021, they spent an average of $1.1 million in development and new construction costs.

According to this release by Chipotle, restaurant level operating margin was 22.6%. I’m using rough numbers here, but 2021 average revenue per restaurant was about $2.54 million dollars. That nets to about $574k.

On about $1.1 million of new build/renovation costs, that nets to about 52% cash on cash returns (pre-tax calculations).

I’d say that’s pretty close. So I can’t say management is trying to hoodwink investors.

More importantly, we now know that Chipotle, at the granular level, is able to reinvest all its profits earned at close to 50% returns on average (pre-tax and capital expenditures etc).

Why is Chipotle’s Base Unit Economics So Important?

Charlie Munger had an insight once that said in the long run, the return an investor gets from a business will roughly equal the return the business itself earns on its capital.

There’s an excellent thread on the dynamics of this by @10-k Diver on twitter and I highly recommend you check it out.

Basically, Chipotle is able to invest $1.1 million into opening a new restaurant and within the first year on average, get back 52% of it. By Year 2, on a very rough basis, the restaurant has paid for itself. By Year 3, everything after operating and maintenance costs drops to the bottom line as profits.

This simple dynamic is why Chipotle has managed to grow revenues 6x and grow net incomes 9x. An unusually high amount. For comparisons sake, Shake Shack, being similarly company operated and similarly American based, increased revenues 12x but still reports negative net income.

Poor restaurant level economics cannot be masked by high revenue growth. The restaurant is the base building block of the business. If that is an unhealthy, cash flow negative business, opening new restaurants rarely lead to better profitability.

Growth Drivers

Return on capital and incremental return on capital will ultimately drive the business profits which in turn drive Chipotle’s share price.

Return on capital and returns on incremental capital invested will also in turn be driven by three more factors:

Chipotle memberships → net sales

Chipotle Digital Kitchens → net margins

Chipotlanes → net sales/margins

Growth Driver (1): Chipotle memberships

Memberships are a new thing but growth in Chipotle loyalty rewards membership is hardly slow starting. Started in March of 19’, Chipotle had approximately 8m loyalty rewards members as of end of the first year and currently has more than 26.5 million members according to their latest transcript. This is important for several reasons.

Frequency & size of ordering → Loyalty Reward members buy more frequently as they get updates and new offerings plus discounts. Transcripts have repeatedly noted loyalty members buy more often, and buy in heavier ticket items.

Easier testing of new menus and flavors before market wide launch → less chances of failure

Greater customer awareness → Apparently, less than 5% of the Chipotle’s customers were familiar with their digital operations pre-2019. This is changing.

Obviously, 26.5m members to send an update out to for new menu items/offerings is a pretty big deal compared to launching it out across restaurants and hoping customers notice.

Edwin Kye in this article noted that members need about 1,250 points to get a free entree which yields to about a 7-8% discount on items bought by loyalty reward members. I don’t know about you → but if there’s a place I love, with food I like, I definitely feel better buying more from that place with a discount/future freebies. This makes Chipotle’s customers stickier. It’s a win win.

Growth Driver (2): Digital Kitchens

Restaurants and eateries are what they are → the formula for profit is basically how many tables you can turn in a day not withstanding take out.

But what if your food is so popular you go from being a restaurant eat-in/take out to being pure take out only?

There are several advantages to this:

Smaller footprint, lesser renovation costs

digital ordering reduces customer friction, so faster transaction time overall, kitchen serves to simply hand over physical goods

higher margins because less space used → less renovation → better effieciency

Chipotle digital kitchens are already up and running and the company is intending to build more wherever the footprint allows.

Growth Driver (3): Chipotlanes/ Drive throughs

Frankly, if you told me adding a drive-through to a food place added a whole new source of profit anywhere in the world, I’d laugh. But in America, it’s apparently quite the thing when nearly everyone owns a car.

According to management, new restaurants with drive throughs/chipotlanes end up getting 15% more sales than average. 15% isn’t chump change when you’re dealing with $2.5 million a year and you’re opening hundreds more restaurants with thousands in the pipeline.

Even better, Chipotlanes enhance cash on cash returns. So the cycle of reinvestment gears up faster.

How Much Can Chipotle Compound At?

To figure out what we should pay, we should figure out how much Chipotle can compound at first.

To figure out how much Chipotle can compound at, we need to figure out the reinvestment rate and the return on incremental capital invested.

And then, we need to marry those assumptions with what the “end-state” of Chipotle will look like, and whether or not the length of our reinvestment runway makes sense.

While it may seem complicated, bear with me, it’s really not.

Chipotle today trades at $1,480.85USD per share, or about 64.66x earnings. With approx $29.85 per share in free cash flow, the stock trades at about 49x free cash flow.

Put another way → that’s so called 50 years to recoup all of your investment, or an approximate return of 2% a year (50 x 2 = 100). Bear in mind, I’m using very rough numbers here.

Here’s the thing about compounders → they don’t look cheap at all often. And often, people feel like the high multiples (of earnings and free cash flow, in this case, 64.66x earnings and 49x free cash flow) mean that the stock has sort of over reached and is “optically” expensive to buy into.

But like I said, we need to look at the compounding rate of the company, the reinvestment opportunities for earnings, and how far the company can go with said reinvestment opportunities to get a clearer view of the picture.

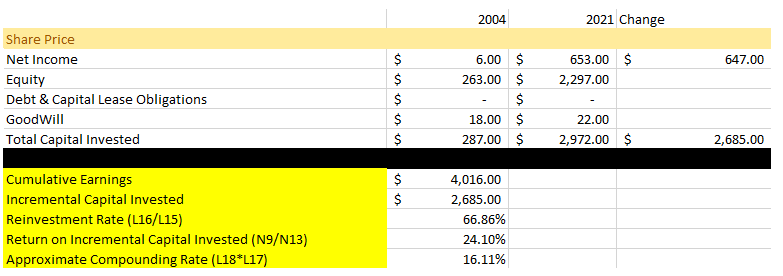

Over here, I’ve attached a very rough outlook on the reinvestment rate and the return on incremental capital.

Per the net income, reinvestment rate over the years has been about 66.86%. Return on that incremental earnings has been about 24.10%. And the approximate compounding rate of the company (reinvestment rate*return on incremental capital invested) should therefore approximate 16.11% with some variance.

Per management call transcripts as of Q42021 here, they think they can operate at least 7,000 Chipotle outlets in America against their current nearly 3,000. Historically, Chipotle has grown store counts at about 1-200 per year. Let’s call it 120. And let’s say we cap Chipotle stores at 6,000 instead of 7,000.

How long can Chipotle compound earnings before it runs out of reinvestment opportunities as it hits max restaurant saturation? The answer is approximately 25 years.

If that is the case,

Now let us look at what Chipotle looks like assuming a below average long term return on capital and return on incremental capital invested, beginning with total capital invested in year 1 reflecting 2021 numbers. And then pushing out to year 25, which is the expected year Chipotle can finish building up restaurants.

At 12% →

Some pointers:

66.86% represents the rough reinvestment rate

Although my above figure puts the return on incremental capital at 24%, I’ve halfed it to 12% to be conservative,

I’ve used 6,000 restaurants expanding at 120 restaurants per year to similarly be conservative about Chipotle’s long term prospects. (Mcdonald’s has 13k outlets, Starbucks has 15k, Subway 21k, and Taco Bell 7k, so with any rational estimate, 6k is a low & reasonable figure).

What do we end up with?

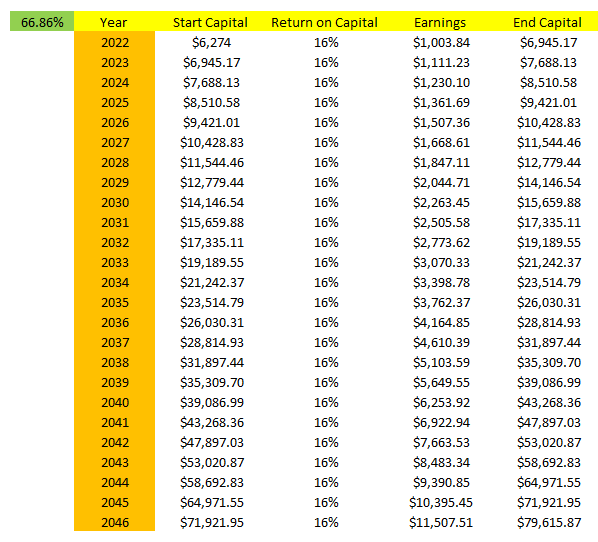

About $4,798.82 in net income by year 25 of our investment.

From here we can try to figure out what our investment would be worth if we assign it a low, mid, and high end multiple.

For reference, this is at 16%. Yes, net income explodes to $11,507M. And this is still underplaying the 24% we calculated return on incremental capital to be at!

How much is Chipotle worth at the end of 25 years to us and what would the rough return rate per year look like?

We ended the above section with two points of data.

At the end of 25 years, we would have;

At 12% return on incremental capital, and 66% reinvestment rate, approximately $4,789.82 in net income.

At 16% return on incremental capital, and 66% reinvestment rate, approximately $11,507.51 in net income.

At current, Chipotle has a market capitalization of $41.49bn. With a current net income of $653M.

This means Chipotle, currently at approximately 63x price to net income.

With $4,789.82 and $11,507.51 in net income, I did a rough look at what we could expect based on low, mid, and high end net income multiples.

Assuming shares outstanding do not move at 29 million shares, this is what we can expect shares to look like given various price to net income multiples per share.

Note that this is pretty nasty. Even with mid end assumptions of 16% return on incremental capital, we will need to see price to net income multiples stay at 70x just to see a 12.44% cagr on our investment. This makes for a poor investment.

Of course, we could go bullish too!

We could assume the following;

10k chipotle restaurants

The full 24% return on incremental capital invested

High price to net income exit multiples

We would almost certainly be able to earn a decent return on capital. I mean, we already have an estimated 12.45% based on just 16% incremental capital returns do we not?

But where would the conservatism be then?

This Is Where Price Matters

I personally aim to compound at approximately 20% per year. Yes, a far goal. But I’d rather aim high and fall slightly short than aim low and achieve it.

Notice what happens when I lower the initial purchase price from $1480.85 to $740.42 which simulates a drop of 50%.

Halving the initial purchase price gives us significantly more room for outperformance. In fact, we start compounding at above 10% once we go past the 20x price to net income multiple, which isn’t too shabby, but isn’t where we want to be just yet.

What happens when we increase our model’s numbers for return on incremental capital to 20% (versus our calculated 24%), and we shift the expected buy price from $1480.85 to $740.42?

Returns actually look far more respectable with 10.41% being the base at 10x price to net income, and surpassing 15.37% at 20x price to net income.

Conclusion

Buy at $740.42.

Assuming 20% return on incremental capital invested, 25 year build out rate, conservative assumptions on total restaurant counts and giving no considerations to;

dividends

buybacks

margin improvements

Chipotlane improving cash on cash returns

Digital kitchens improving margins

We can safely assume that at $740 or about -50% from here, we will likely have a more than good chance of seeing 15.37% returns or higher on our invested capital.

Some of this is good and pretty insightful. It is a good reminder to see just how extreme expectations need to be to support a multiple of almost 70.

However, a few things. First of all, this is a bit of a nitpick, but I can't stand seeing numbers to 4 or 5 significant figures when for all we know they could be 20% or 30% off. It conveys a sense of accuracy we really don't have.

Second, you need to account for what they do with the cash they don't reinvest when you do the total rate of return calculation. If they didn't reinvest any, the rate of return would not be zero. It would be the equal to the dividend yield, which is 1/PE * (1-reinvestment rate) = 1/65 * 0.33 = 0.5%, which we would add onto that 12.4% to get 12.9%. So in this case not too impactful, but always worth considering. A business that can grow 10% YOY while investing 100% of profits is a lot less valuable than one that can do so while investing only 20% of profits, and paying the rest out in dividends or buybacks.

Third, you use a linear model for the number of locations to calculate how long they can keep expanding, but then use an exponential model for earnings, which implicitly assumes an exponential number of locations. That's quite a convoluted way of saying it, so I'll try to explain another way. If they keep building 120 restaurants per year, right now their restaurant count would be increasing by about 4% YOY, but by the time they're at 7000 restaurants, 120 per year is only 1.7% growth in store count. Therefore, their reinvestment rate will drop significantly.

If you need another clue that your model is fundamentally flawed, notice that the further you reduce the number of stores built per year, the more their apparent intrinsic value goes up, because their earnings can keep compounding at the rate you calculated for longer. What's going on here? The issue is you're using separate models of store count and earnings/cash flow, with no feedback between them. You need one iterative model where the number of restos influences earnings, and potentially earnings also influence the number of restaurants. You can project that forwards in time and get much more sensible numbers, as long as you account for how return on incremental capital will decrease as the market becomes saturated, and their reinvestment rate will also decrease as they begin to find it harder to find places to put a larger amount of earnings.

In any case though, I don't think you need any kind of model to realise that buying an already-large restaurant chain for 65x earnings is incredibly risky and daft.